Summary

- Payday advances come at an extreme cost – with effective annual interest rates between 300-600%, they're designed for very short-term use only, not as ongoing financial solutions.

- The debt cycle is real and dangerous – over half of payday borrowers take multiple loans per year, often paying more in fees than the original loan amount.

- Alternatives exist for all situations – from community resources to banking products, better options are available even for those with credit challenges.

- Homeowners have a powerful alternative in secured home loans, which offer lower rates, larger amounts, and flexible approval criteria that focus on home equity rather than credit score.

Are you caught in a financial squeeze between paychecks?

That urgent car repair or unexpected medical bill won't wait, but neither will your landlord or grocery needs. For many Canadians facing these tight spots, payday advances seem like a quick fix – but they often create more problems than they solve.

In this comprehensive guide, you'll discover:

- The hidden costs behind those "quick and easy" payday advance promises

- Province-by-province regulations that affect what lenders can charge you

- More innovative alternatives that won't trap you in a cycle of debt – even if you have credit challenges

By the way — stuck in the payday loop? If you’re a homeowner, you may be able to replace payday advances with a single payment using your home equity. Lotly looks at the full picture (including unconventional income) to help you build a realistic plan, not a two-week deadline. Book a free consultation to see your options.

What is a Canadian payday advance?

A payday advance is a short-term, high-cost loan designed to bridge the gap between paychecks when unexpected expenses arise. Unlike traditional loans that charge interest over time, payday advances typically charge a flat fee based on the amount borrowed.

These loans are meant to be a temporary solution – a financial band-aid until your next payday arrives. However, the simplicity and accessibility that make them appealing often mask their significant downsides.

Key characteristics of payday advances:

- Loan amounts: Typically range from $100 to $1,500

- Repayment period: Usually 14-62 days (coinciding with your pay cycle)

- Fee structure: Flat fees rather than traditional interest rates

- Security required: Post-dated check or pre-authorized debit

- Credit check: Minimal or none, making them accessible to those with poor credit

While payday advances may seem straightforward, their fee structure often obscures the true cost of borrowing. When calculated as an annual percentage rate (APR), the fees can translate into interest rates of 300% to 600% — far higher than credit cards, personal loans, or even cash advances on credit cards. Luckily, the legal cap on fees is $14 per $100 borrowed, but if you’re getting a bridge for every payday… it starts to add up.

How Canadian payday advances work

Before considering a payday advance, it's essential to understand precisely how these financial products function and what you'll need to qualify. The process is designed to be quick but comes with high costs that aren't always obvious at first glance.

Requirements to qualify

Payday lenders typically have minimal qualification requirements compared to traditional financial institutions. This accessibility is part of their appeal, especially for those with limited options.

To qualify for a payday advance in Canada, you'll typically need:

- Proof of regular income: Recent pay stubs or benefit statements

- Active bank account: At least 3 months old in most cases

- Permanent Canadian address: Proof of residency

- Valid ID: Government-issued photo ID (and be at least 18 years old)

- Contact information: Phone number and email address

Unlike traditional loans, payday lenders rarely perform thorough credit checks. Instead, they focus on verifying your income and ability to repay on your next payday.

The application process

The payday advance process is designed to be quick and convenient, a major selling point for those facing urgent financial needs.

Online application:

- Complete a simple online form with personal and financial information

- Upload or email required documentation (ID, proof of income, bank statements)

- Receive approval decision, often within minutes to hours

- Accept loan terms electronically

- Receive funds via direct deposit, often within 24 hours

In-store application:

- Visit a payday loan store location

- Bring required documentation

- Complete application with staff assistance

- Receive approval decision on the spot

- Leave with cash or a loaded prepaid card

The speed and simplicity of this process make payday advances tempting when you're facing urgent expenses. However, this convenience comes at a high cost — you must understand it before signing any agreement.

Repayment terms and conditions

The repayment structure of payday advances is what often leads borrowers into financial difficulty. Understanding these terms is crucial before taking out a loan.

- Repayment method: Pre-authorized debits from your bank account or post-dated checks

- Due date: Typically, your next payday (14-30 days from receiving the loan)

- Full repayment required: Unlike credit cards or lines of credit, the entire loan amount plus fees must be repaid at once

- Rollover options: Some provinces allow extensions or rollovers for additional fees

- Consequences of non-payment: NSF fees, late charges, collection activities, and damage to your credit score

The one-time repayment structure is where many borrowers encounter problems. If you borrow $500 to cover an emergency expense, you'll need to repay $575-$585 (at typical rates) from your next paycheck. If that paycheck is already allocated to rent, utilities, and groceries, you may find yourself short again – leading to a cycle of repeated borrowing.

The true cost of payday advances in Canada

Payday advances are among the most expensive borrowing options available to Canadians. Understanding the whole cost structure helps you make an informed decision about whether this type of loan makes financial sense for your situation.

Fee structure and interest rates

Payday lenders typically charge a flat fee per $100 borrowed rather than a traditional interest rate. This structure can make the costs seem reasonable at first glance, but when converted to an annual percentage rate (APR), the true cost becomes apparent.

Provincial maximum fees:

- Provinces cap fees at $14 per $100 borrowed

- This translates to APRs of approximately 300-600%

- Additional fees may apply for late payments or NSF checks

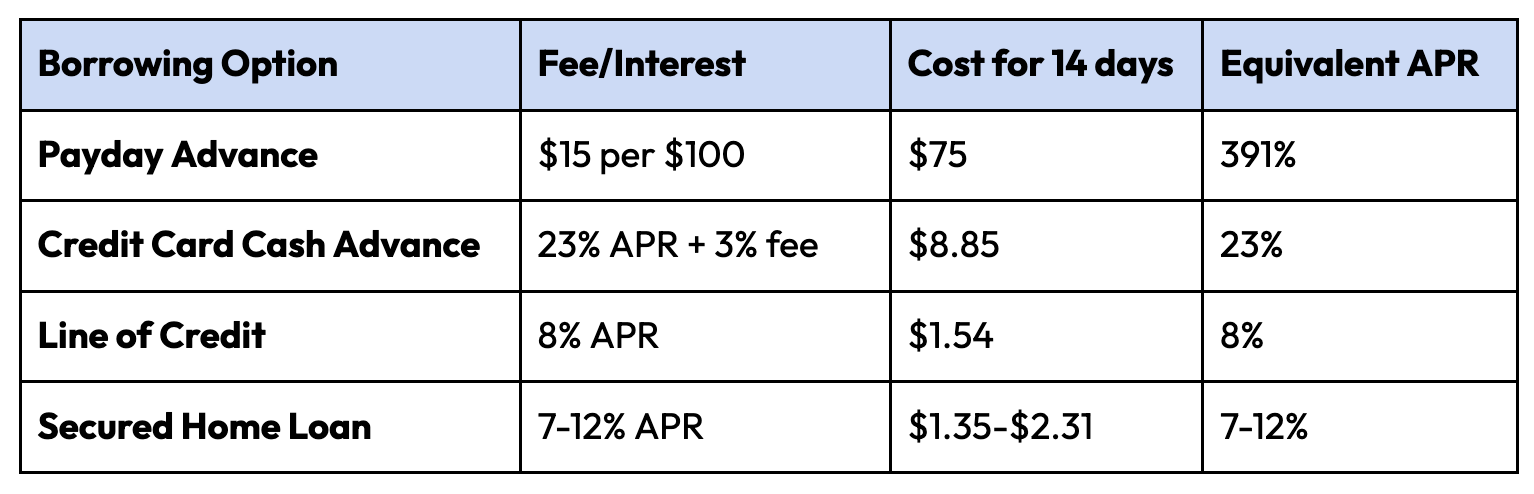

To put this in perspective, consider borrowing $500 for 14 days (we’ll use $15 as an illustrative fee since it’s a cleaner number):

The difference is dramatic – what seems like a modest $75 fee represents an interest rate many times higher than other financial products.

The debt cycle risk

The most significant danger of payday advances isn't just their high cost for a single loan; it's the potential to trap borrowers in an ongoing cycle of debt.

How the cycle works:

- You borrow $500 to cover an unexpected expense

- On your next payday, you owe $575 (with a $15/$100 fee)

- After paying rent and essential bills, you can't afford the full $575

- You pay a fee to extend the loan or take out a new loan to cover the old one

- Two weeks later, you're in the same position, but now with additional fees

The statistics are concerning:

- FCAC found that only 48% were repaid by the next paycheque, 30% had difficulty repaying on time, and 7% took another payday loan to pay the first

- Repeat use is common — about half of borrowers are repeat users over a multi-year window

- Some borrowers end up paying more in fees than the original loan amount

Example scenario: Sarah borrows $400 for car repairs. On her next payday, she can't afford the full $460 repayment, so she pays $60 to extend the loan. This pattern continues for three months, with Sarah paying $60 every two weeks. After finally repaying the loan, she's spent $400 in principal plus $240 in fees – a 60% cost for a three-month loan.

Provincial regulations for payday advances

Canada's provinces have implemented various regulations to protect consumers from predatory lending practices. These rules vary by location and affect the maximum costs and terms of payday advances.

Provincial regulations typically cover:

- Maximum fees lenders can charge

- Cooling-off periods that allow borrowers to cancel loans without penalty

- Restrictions on rollovers or concurrent loans

- Mandatory disclosure of loan terms and costs

- Requirements for installment repayment plans for repeat borrowers

While these regulations provide some protection, the fundamental structure of payday advances (high fees and short repayment periods) remains essentially unchanged. Even at the maximum legal rates, these loans remain significantly more expensive than alternatives.

Smart alternatives to Canadian payday advances

Before turning to a high-cost payday advance, consider these alternatives that could save you significant money and help avoid the debt cycle. Many options exist even for those with credit challenges.

Traditional banking options

Even with credit challenges, several traditional banking products offer better terms than payday advances:

- Personal lines of credit: Ongoing access to funds with interest charged only on what you use

- Overdraft protection: Covers shortfalls in your checking account at much lower rates than payday loans

- Credit card cash advances: While not ideal, they typically charge 19-23% APR plus a one-time fee of 1-3%

- Small personal loans: Many credit unions offer small-dollar loans with reasonable rates and terms

Community resources

Several community-based options can help during financial emergencies:

- Credit union programs: Many credit unions offer emergency loan programs with counselling services

- Community assistance programs: Local non-profits may provide emergency assistance for utilities, food, or housing

- Non-profit lending circles: Peer-to-peer lending groups that offer interest-free loans to members

- Government assistance: Provincial and federal programs may provide emergency support

Homeowner? Home equity can be a lower-cost alternative to payday advances — especially if your credit or income isn’t ‘perfect on paper.’ Lotly specializes in home equity loans & HELOCs with flexible qualification. Book a free consultation to see if it’s the right fit.

Using home equity as a smarter solution

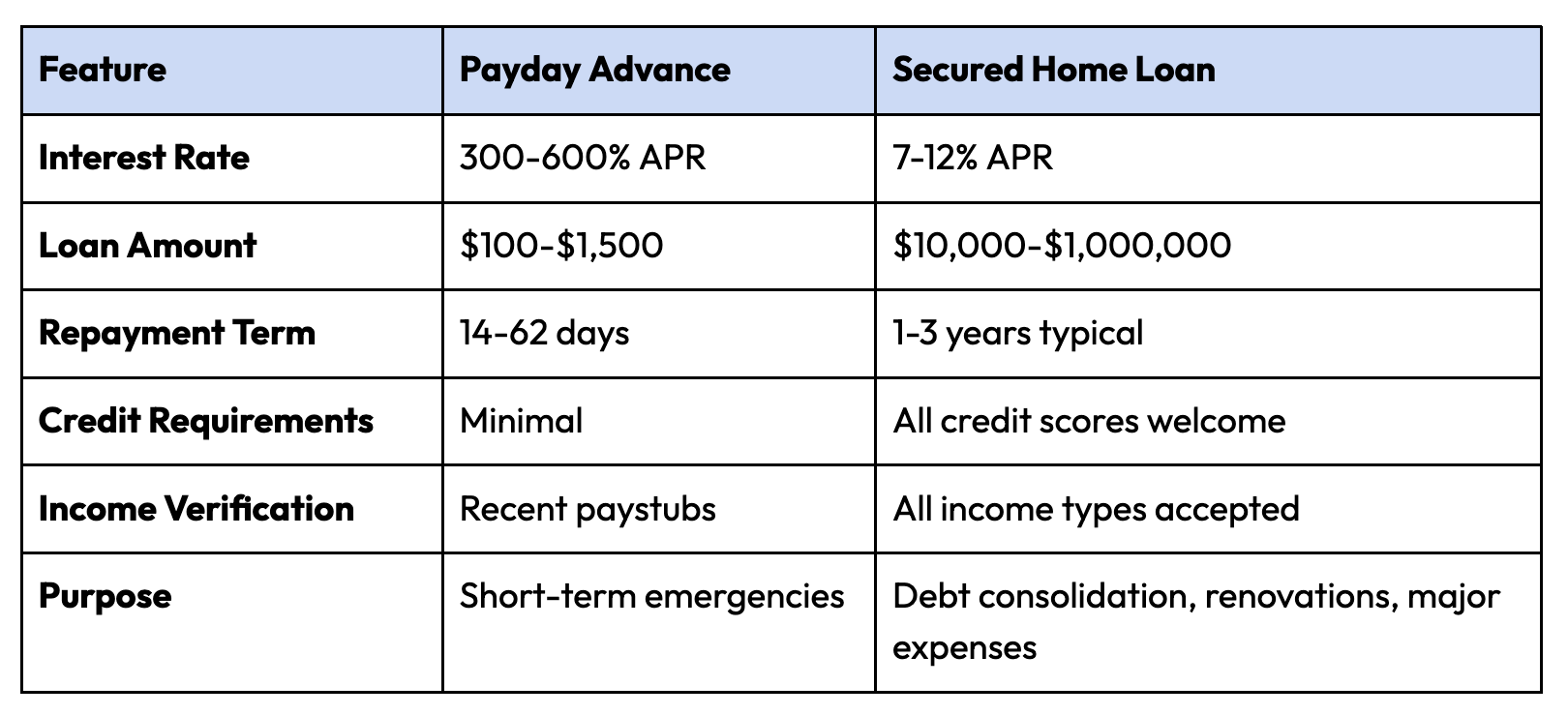

For homeowners facing financial challenges, leveraging your home equity can provide a much more affordable alternative to payday advances. Secured home loans help Ontario homeowners access funds at significantly lower rates than payday advances, even for those with credit challenges.

How secured home loans compare to payday advances:

Benefits of using a secured home loan:

- Consolidate high-interest debts: Replace multiple payments (including payday loans) with one manageable monthly payment

- Lower overall interest costs: Save thousands in interest compared to payday advances or credit cards

- Improve monthly cash flow: Reduce total monthly payments by spreading repayment over a longer term

- Break the debt cycle: Create a sustainable repayment plan rather than a two-week deadline

- Build credit: Regular payments on a secured loan can help rebuild your credit score

Example: Let’s say Michael had accumulated $15,000 in credit card debt and had taken out payday loans twice to make minimum payments. His monthly payments totalled $850, and he was barely keeping up. By using a secured home loan, he consolidated all his debts into a single $425 monthly payment, immediately improving his cash flow by $425 per month while paying a much lower interest rate.

Warning signs of predatory payday lenders

Not all payday advance providers operate with the same level of transparency. Learn to identify red flags that may indicate predatory lending practices.

When considering a payday advance, watch for these warning signs:

- Unlicensed operations: Legitimate lenders must be licensed in your province

- Hidden fees or unclear terms: All fees should be clearly disclosed upfront

- Pressure to borrow more than needed: Some lenders encourage larger loans to collect more fees

- No verification of ability to repay: Responsible lenders assess whether you can realistically repay

- Aggressive collection tactics: Threats, excessive calls, or contacting your employer are red flags

- No cancellation option: Provincial regulations require a cooling-off period

Always verify a lender's license status with your provincial consumer protection office before borrowing, and read all terms carefully before signing any agreement.

Steps to break the payday loan cycle

If you're already caught in a cycle of payday borrowing, these strategies can help you regain control of your finances and find a path forward.

Breaking free from the payday loan cycle requires a deliberate approach and often some short-term sacrifices. Here's how to get started:

- Stop the cycle immediately: Avoid taking out new payday loans while working on your exit strategy

- Create a realistic budget: Track all income and expenses to identify potential savings

- Prioritize essential expenses: Focus on housing, food, utilities, and transportation first

- Negotiate with current payday lenders: Many will accept extended payment plans if approached proactively

- Consider debt consolidation options: For homeowners, a secured home loan can provide immediate relief by consolidating payday loans and other debts into one affordable payment.

- Build an emergency fund: Start with $500- $1,000 to cover minor emergencies without borrowing.

- Seek credit counselling: Non-profit credit counsellors can provide personalized advice and debt management plans.

Pro Tip: When consolidating payday loans with a secured home loan, make sure the lender accepts all credit scores and income types. This ensures you won't face rejection based on credit challenges that may have led to payday borrowing in the first place.

Making the right financial decision for your situation

Every financial situation is unique. This section helps you evaluate whether a payday advance makes sense for your specific circumstances or if another option would better serve your needs.

Before making any borrowing decision, ask yourself these key questions:

- Is this expense truly urgent? Can it be delayed until your next payday?

- Have I explored all alternatives? Including payment plans, community assistance, or family help?

- Can I realistically repay this loan on my next payday? Consider your upcoming bills and expenses.

- What would happen if I couldn't repay on time? Do you have a backup plan?

- For homeowners: Have I considered using my home equity instead of high-cost short-term loans?

Calculate the true cost: For a $500 payday advance with a $15 per $100 fee:

- Initial cost: $75 ($500 × 15%)

- If extended for 3 months (6 pay periods): $450 in fees

- Total cost: $950 for a $500 loan

Ready to break free from payday loans? Lotly can help

Understanding the true cost of payday advances is the first step toward making better financial decisions. For homeowners, there's a clearer path forward that doesn't involve triple-digit interest rates or two-week repayment deadlines.

Key takeaways:

- Payday advances come at an extreme cost – with effective annual interest rates between 300-600%, they're designed for very short-term use only, not as ongoing financial solutions.

- The debt cycle is real and dangerous – over half of payday borrowers take multiple loans per year, often paying more in fees than the original loan amount.

- Alternatives exist for all situations – from community resources to banking products, better options are available even for those with credit challenges.

- Homeowners have a powerful alternative in secured home loans, which offer lower rates, larger amounts, and flexible approval criteria that focus on home equity rather than credit score.

Ready to get out of payday advances for good? If you’re a homeowner, Lotly can help you explore home equity options that consolidate high-cost debt into a clearer, more manageable plan — with flexible consideration for income sources banks often ignore. Book a free consultation to understand your options.

Ayaz Virani

Ayaz Virani is the Vice President of Sales at Lotly and a licensed mortgage agent in Ontario under 8Twelve Mortgage Corporation (FSRA License #13072). With over three years of experience as a Growth Manager at KOHO Financial, Ayaz brings deep expertise in helping Canadians access smart, flexible financing. He has successfully funded hundreds of homeowners and is known for his transparent advice, fast service, and genuine care for each customer’s financial goals.