Summary

- Understand GIC rate tiers to maximize your returns by strategically investing amounts that reach critical thresholds, potentially earning hundreds more in interest.

- Implement a GIC ladder strategy to balance liquidity needs with higher returns, ensuring you always have funds maturing while maintaining exposure to longer-term rates.

- Consider registered accounts first for your GIC investments, particularly TFSAs, to shield your interest earnings from taxation and maximize your after-tax returns.

- Look beyond the big banks for your GIC investments, as online banks and credit unions typically offer significantly higher rates that can substantially increase your returns over time.

If you’ve been ignoring GICs because they felt outdated, 2026 has changed the math.

Some of the highest posted GIC rates in Canada are back in the 3.6%–3.9% range, offering welcome returns at a time when many Canadians are tired of market volatility. But pick the wrong term, miss a better provider, or ignore tax and insurance rules, and you can quietly lose a meaningful portion of your return.

This guide shows you how to choose GICs the right way:

- What GICs are and how returns are actually calculated

- Where the best GIC rates in Canada tend to come from

- Which GIC types make sense for different goals

- How to compare rates properly (APY, compounding, flexibility)

P.S. — If your cash is tied up in GICs but you want flexibility without breaking a term early, some Canadians pair guaranteed returns with a home-equity option. Lotly helps homeowners access their equity—often using income sources traditional lenders ignore. Book a free consultation to learn more.

What are GICs and how do they work?

Guaranteed Investment Certificates (GICs) are among Canada's most popular low-risk investment options. These financial products offer a guaranteed return on your investment over a specified term, providing peace of mind for conservative investors and those looking to diversify their portfolios with stable, predictable assets.

When you purchase a GIC, you're essentially lending your money to a financial institution for a predetermined period. In exchange, they guarantee to return your principal plus interest at the end of the term. This straightforward arrangement makes GICs an attractive option for many Canadians seeking financial security.

Basic definition and function of GICs

A GIC is a secure investment product where you deposit a fixed amount of money for a specific term (ranging from 30 days to several years), and in return, you receive a guaranteed interest rate. Unlike more volatile investments like stocks or mutual funds, GICs provide certainty about your returns from day one.

How interest is calculated and paid

GICs typically offer two main interest calculation methods:

- Simple interest: Interest is calculated only on your initial investment and paid at maturity or at regular intervals.

- Compound interest: Interest is calculated on both your initial investment and any interest already earned, potentially increasing your returns over time.

Most financial institutions offer interest payment options, including:

- Paid at maturity: All interest is paid when your GIC term ends

- Annual payment: Interest is paid once per year

- Semi-annual/quarterly/monthly: Interest is paid at more frequent intervals, providing regular income

Minimum investment requirements

Most Canadian financial institutions require a minimum investment for GICs, typically ranging from:

- Big banks: $500-$1,000 minimum

- Online banks: Often as low as $100

- Credit unions: Usually $500-$1,000, but can vary by institution

Safety and insurance through CDIC

One of the most appealing aspects of GICs is their safety. GICs purchased from member institutions are protected by the Canada Deposit Insurance Corporation (CDIC) for up to $100,000 per depositor per insured category. Credit union GICs are typically protected by provincial deposit insurance corporations, often with even higher coverage limits.

Current GIC rates in Canada (2026)

The GIC market is constantly evolving, with rates fluctuating in response to economic conditions, Bank of Canada policy decisions, and competition among financial institutions. Generally, you'll find significant variations between the rates offered by traditional banks, online banks, and credit unions.

Big five bank GIC rates

Canada's major banks typically offer lower GIC rates than online banks and credit unions, but they offer the convenience of integrated banking services and branch access. Rates at the Big Five banks include:

While specific rates change frequently, these traditional banks generally offer rates ranging from 1.00% to 4.50%, depending on term length, with longer terms typically providing higher rates.

Online bank GIC rates

Online banks consistently offer some of the most competitive GIC rates in Canada due to their lower overhead costs. These digital-first institutions include:

Online banks frequently offer rates 0.50% to 1.50% higher than traditional banks across all term lengths, making them attractive options for rate-conscious investors.

Credit union GIC rates

Credit unions often provide excellent GIC rates that compete with or exceed those of online banks, particularly for members or local residents. Notable credit unions include:

*May include promotional rates

Many credit unions offer promotional rates throughout the year, sometimes exceeding even the best online bank offerings by 0.25% to 0.75%.

Types of GICs available in Canada

Understanding the various types of GICs available can help you select the investment option that best aligns with your financial goals and needs.

Term length options

The term length you choose significantly impacts both your interest rate and your access to funds:

Short-term GICs: 30 days to 1 year

- Benefits: Provide flexibility and liquidity. Typically offer lower interest rates, but allow you to reinvest at potentially higher rates if interest rates rise.

- Best for: Emergency funds, saving for near-term goals, or when you expect interest rates to increase soon.

Mid-term GICs: 1-3 years

- Benefits: Strike a balance between competitive rates and reasonable access to your money. Often provide a sweet spot in the rate structure.

- Best for: Saving for goals 1-3 years away, like a down payment or major purchase.

Long-term GICs: 3-5+ years

- Benefits: Typically offer the highest interest rates. Require you to lock in your money for extended periods. Provide stability and predictable returns over a longer investment horizon.

- Best for: Long-term financial goals when you're confident you won't need the funds before maturity.

Registered vs. non-registered GICs

The registration status of your GIC affects how your investment returns are taxed:

TFSA GICs:

- GICs held within a Tax-Free Savings Account (TFSA) allow your interest to grow completely tax-free. This makes TFSA GICs particularly attractive for most investors, as you'll never pay tax on the interest earned

- Best for: Most investors looking to maximize after-tax returns

RRSP GICs:

- GICs held within a Registered Retirement Savings Plan (RRSP) allow interest to grow tax-deferred until withdrawal. Your contributions may also provide an immediate tax deduction.

- Best for: Retirement savings and tax deferral strategies.

RESP GICs:

- GICs held within a Registered Education Savings Plan (RESP) allow interest to grow tax-deferred until withdrawal for educational purposes. These can also qualify for government education grants.

- Best for: Saving for a child's education expenses.

Non-registered GICs and Tax Implications:

- In non-registered accounts, GIC interest is fully taxable, and for many compound / paid-at-maturity GICs, you report interest each complete investment year (not just at maturity).

- Best for: Investors who have maximized their registered account contribution room or need access to funds without withdrawal restrictions.

Specialty GIC products

Financial institutions offer several specialized GIC products to meet diverse investor needs:

Cashable/Redeemable GICs

- These GICs allow you to access your money before maturity, typically after a minimum holding period (often 30-90 days). The trade-off is a lower interest rate compared to non-redeemable GICs.

- Best for: Investors who value flexibility and may need access to their funds

Market-linked GICs

- These hybrid products offer potential returns tied to market performance (often stock market indices) while guaranteeing your principal. Returns can be higher than those of traditional GICs, but are not guaranteed beyond the minimum rate.

- Best for: Investors seeking higher potential returns with principal protection.

Escalating Rate GICs

- These GICs feature interest rates that increase at predetermined intervals throughout the term. They provide lower returns initially but higher rates in later years.

- Best for: Investors who want to lock in for longer terms while seeing their returns increase over time.

Foreign Currency GICs

- Available in currencies like USD or EUR, these GICs allow you to earn interest while maintaining exposure to foreign currencies.

- Best for: Investors looking to diversify currency exposure or planning future expenses in another currency.

Factors that affect GIC rates in Canada

Understanding what influences GIC rates can help you time your investments more effectively and set realistic expectations for returns:

- Bank of Canada interest rate decisions. The Bank of Canada's policy interest rate has the most direct impact on GIC rates. When the central bank raises rates, financial institutions typically follow by increasing their GIC rates, and vice versa when rates are lowered.

- Economic conditions and inflation. Broader economic factors, particularly inflation, significantly influence GIC rates. During periods of higher inflation, financial institutions often raise GIC rates to attract deposits and ensure real returns remain positive after accounting for inflation.

- Financial institution competition. Competition among banks, credit unions, and other financial institutions can drive rates higher as they vie for deposits. This is why online banks and credit unions, which often compete aggressively for market share, frequently offer better rates than established big banks.

- Term length. Longer terms typically offer higher rates to compensate investors for committing their money for extended periods. This creates a "yield curve," where rates increase as term length increases.

- Investment amount. Many institutions offer tiered rates based on investment amount, with higher rates for larger deposits. Standard threshold amounts include $5,000, $25,000, $100,000, and $1,000,000.

- Special promotional offers. Financial institutions regularly offer promotional rates that exceed their standard offerings. These limited-time offers can provide exceptional value but require timely action to secure.

How to compare GIC rates effectively

Looking beyond the advertised percentage rate is crucial when comparing GIC options. Here's how to evaluate GICs comprehensively:

- Understanding annual percentage yield (APY) vs. simple interest. Annual Percentage Yield (APY) accounts for the effect of compounding, giving you a more accurate picture of your actual returns compared to simple interest rates. When comparing GICs, always look for the APY to make fair comparisons.

- Considering compounding frequency. The frequency of interest compounding can significantly impact your returns. More frequent compounding (monthly vs. annually, for example) results in higher effective returns even with the same stated interest rate.

- Evaluating early redemption penalties and flexibility. For non-redeemable GICs, understand the penalties or restrictions if you need your money before maturity. Some institutions prohibit early redemption entirely, while others charge substantial penalties that can erase your interest earnings.

- Assessing minimum investment requirements. Lower minimum investments provide more flexibility for smaller investors or those who want to spread their money across multiple GICs. Consider whether higher minimums for premium rates align with your investment capacity.

- Comparing CDIC coverage limits. While standard CDIC coverage protects up to $100,000 per depositor per insured category, some credit unions offer higher coverage through provincial insurance programs. This becomes particularly important for larger investments.

Homeowner note: If you’re building a GIC plan but worried about needing cash unexpectedly, you can set up a “liquidity backstop,” so you’re not forced to break a GIC early. Lotly helps homeowners explore home equity options that fit real-world income situations (including non-traditional sources). Book a free consultation to see what’s realistic for you.

4 strategies to maximize your GIC returns

Implementing strategic approaches to GIC investing can significantly enhance your overall returns while maintaining the security these investments are known for.

#1. GIC laddering

GIC laddering is one of the most effective techniques for balancing access to funds with competitive returns.

Definition and benefits of GIC laddering

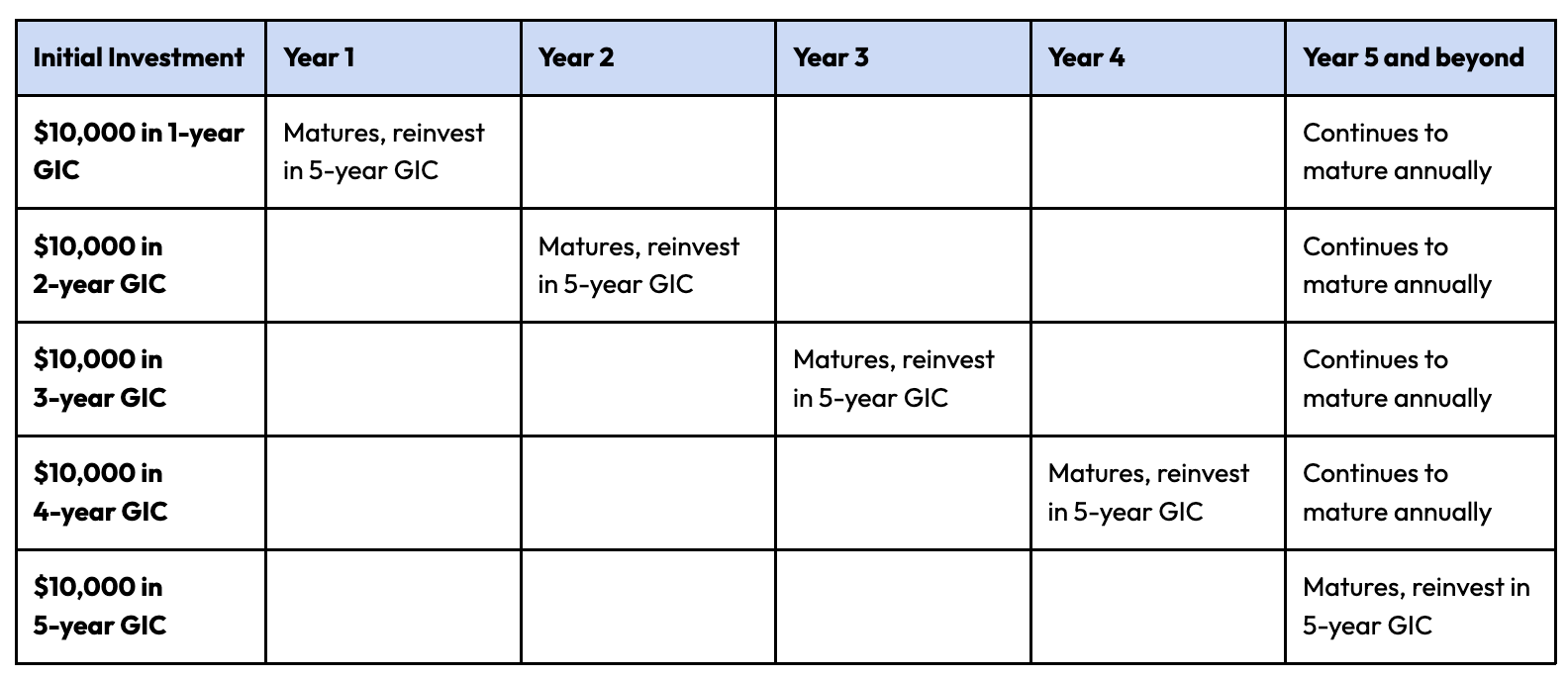

A GIC ladder involves dividing your investment into equal portions and investing them in GICs with staggered maturity dates. As each GIC matures, you reinvest it into a new long-term GIC, maintaining the ladder structure.

The key benefits include:

- Regular access to funds as GICs mature at planned intervals

- Higher average returns by always having some money in longer-term, higher-rate GICs

- Protection against interest rate fluctuations by regularly reinvesting at current rates

Step-by-step guide to creating a GIC ladder

- Determine your total investment amount and divide it into equal portions (typically 5 portions for a standard ladder)

- Invest each portion in GICs with consecutive term lengths (e.g., 1, 2, 3, 4, and 5 years)

- When the 1-year GIC matures, reinvest it in a new 5-year GIC

- Continue the pattern as each GIC matures, continually reinvesting in a new 5-year term

- After 4 years, your ladder is fully established with a GIC maturing every year

Example of a 5-year GIC ladder structure

For a $50,000 investment divided into five $10,000 portions:

Once fully established, you'll have $10,000 becoming available each year while maintaining the higher average interest rate of 5-year terms.

Pro tip: keep your ladder intact. The biggest ladder-killer is an emergency that forces you to cash out early. If you’re a homeowner, a home equity option can sometimes cover large one-off costs, so your GIC ladder keeps compounding. Talk to Lotly to understand what you may qualify for.

#2. Rate negotiation

Many investors don't realize that GIC rates are often negotiable, especially for larger deposit amounts.

- Do your research before approaching your financial institution

- Speak with a manager or investment specialist rather than a frontline teller

- Be prepared to transfer your business if necessary

- Highlight your overall relationship with the institution, including other accounts and services

- Ask directly for a better rate, citing competitor offerings

- Bring printed or digital evidence of better rates from competitors when negotiating. Financial institutions often have "rate match" or "rate beat" policies that may not be advertised but can be accessed when challenged with competitor offers.

#3. Timing your GIC purchases strategically

Consider these timing strategies:

- Purchase before expected rate decreases to lock in higher rates

- Use short-term GICs during rising rate environments to maintain flexibility

- Buy during promotional periods when institutions offer special rates

- Align purchases with fiscal year-ends when financial institutions may be more motivated to attract deposits

#4. Combining GICs with other investments

GICs work best as part of a diversified investment strategy rather than in isolation.

Creating a balanced portfolio with GICs and other assets

Consider allocating your investments across different asset classes:

- GICs and high-interest savings for capital preservation and stability

- Bonds for moderate risk and income

- Stocks or equity ETFs for long-term growth

- Real estate for diversification and potential income

The appropriate allocation depends on your risk tolerance, time horizon, and financial goals.

Using GICs as the safe portion of your investment strategy

Many financial advisors recommend using GICs for:

- Emergency funds (using cashable GICs)

- Short-term savings goals (1-5 years)

- The conservative portion of retirement portfolios

- Income generation for retirees or those needing a predictable cash flow

Alternatives to consider alongside GICs

While GICs offer security and guaranteed returns, consider complementing them with:

- High-interest savings accounts for immediate liquidity

- Bond ETFs for potentially higher yields with moderate risk

- Dividend stocks for income and growth potential

- Real estate investments for diversification

How to purchase GICs in Canada

The process of buying GICs varies slightly depending on your chosen financial institution and purchase method.

Online banking purchase process

Most major financial institutions offer a streamlined online process:

- Log in to your online banking portal

- Navigate to the investments or GIC section

- Select the GIC type, term, and interest payment option

- Choose the source of funds (existing account or new deposit)

- Review and confirm the investment details

- Complete the purchase and save your confirmation

The entire process typically takes less than 10 minutes if you're already set up for online banking.

In-branch application process

For those who prefer face-to-face service:

- Schedule an appointment with a financial advisor (recommended but not always required)

- Bring identification and account information

- Discuss your investment goals and GIC options

- Complete the application forms

- Fund the GIC from your existing account or a new deposit

- Receive your GIC certificate or confirmation

In-branch purchases offer the advantage of personalized advice and the potential to negotiate rates.

Through investment advisors or brokers

Working with an investment professional offers additional benefits:

- Consult with your advisor about your investment goals

- Review GIC options from multiple financial institutions

- Select the most appropriate GIC(s) based on your needs

- Complete the required paperwork (often handled by the advisor)

- Transfer funds to purchase the GIC(s)

- Integrate the GIC into your overall investment strategy

Investment advisors can often access GICs from multiple institutions, potentially finding better rates than those available from a single bank.

Required documentation and information

To purchase a GIC, you'll typically need:

- Government-issued photo ID (driver's license, passport)

- Social Insurance Number (SIN)

- Banking information for the source of funds

- Investment amount and term decision

- Beneficiary information (optional but recommended)

Account options for holding GICs

GICs can be held in various account types, each with different implications:

- Registered accounts (TFSA, RRSP, RESP, RRIF)

- Non-registered personal accounts

- Joint accounts

- Corporate accounts (for businesses)

- Trust accounts (formal or informal)

Choose the account type that best aligns with your tax planning and financial goals.

GIC rate trends and forecasts for 2026-2027

Understanding historical patterns and current economic factors can help inform your GIC investment decisions.

Historical GIC rate trends in Canada

GIC rates have historically followed a cyclical pattern, influenced by broader economic conditions and monetary policy. Over the past decade, we've seen periods of both historically low rates and more recent increases as central banks combat inflation.

Relationship between Bank of Canada policy and GIC rates

The Bank of Canada's overnight rate serves as the foundation for various interest rates throughout the economy. When the central bank raises its policy rate to combat inflation, GIC rates typically follow suit, though not always immediately or proportionally.

Financial institutions consider multiple factors when setting GIC rates, including:

- Current and anticipated policy rates

- Yield curve expectations

- Competitive positioning

- Funding needs

- Economic outlook

Expert predictions for interest rate movements

While specific predictions vary, financial analysts generally expect:

- Stabilization of interest rates following the inflation-fighting cycle

- Gradual adjustments based on economic indicators

- Continued competition among financial institutions for deposits

These factors suggest that GIC investors should stay informed about economic developments and be prepared to adjust their strategies accordingly.

Strategies for investing during changing rate environments

Different rate environments call for different GIC strategies:

In rising rate environments:

- Consider shorter terms to maintain flexibility

- Use a GIC ladder to regularly reinvest at higher rates

- Look for special features like rate escalation or market-linked returns

In falling rate environments:

- Lock in longer terms to preserve current higher rates

- Consider locking in promotional rates when available

- Compare cashable vs. non-cashable options carefully

In stable rate environments:

- Focus on optimizing your ladder structure

- Negotiate more aggressively with financial institutions

- Compare rates across a broader range of institutions

The hidden opportunity in tiered GIC tates

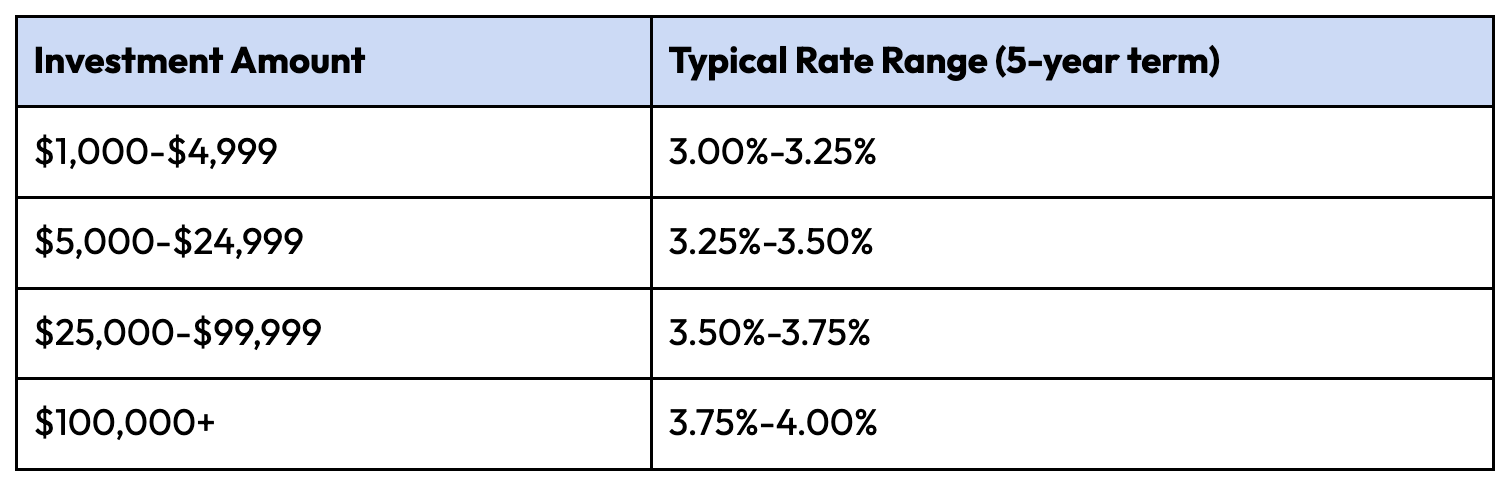

One often overlooked aspect of GIC investing is understanding and leveraging tiered rate structures. Many financial institutions offer significantly better rates for larger investments, creating what we call "rate thresholds."

Understanding rate thresholds

Rate thresholds are specific investment amounts at which financial institutions offer higher interest rates. Common thresholds include $5,000, $25,000, $100,000, and sometimes $1,000,000.

For example, investing $4,900 might earn you 3.25%, but adding just $100 more to reach the $5,000 threshold could bump your rate to 3.50%. This slight difference can translate to significant additional earnings over the term of your investment.

The threshold calculator

Use this simple formula to determine if adding funds to reach the next tier is worth it:

Additional Interest Earned = (Higher Tier Rate - Lower Tier Rate) × (New Investment Amount) × (Term in Years)

Example calculation:

- Current investment: $4,900 at 3.25% for 5 years

- Adding $100 to reach $5,000 at 3.50% for 5 years

- Additional interest: (3.50% - 3.25%) × $5,000 × 5 = 0.25% × $5,000 × 5 = $62.50

In this case, adding just $100 would earn you an additional $62.50 in interest over the 5-year term.

Real-world threshold examples

Here's how tiered rates might typically be structured across different investment amounts:

These differences may seem small, but they can add up to hundreds or even thousands of dollars in additional interest over the investment term.

The "split investment myth"

Many investors believe that splitting investments between multiple institutions to chase the "best rates" is always optimal. However, this strategy often underperforms a single larger investment at a tiered rate when accounting for:

- The higher tier rate that comes with larger deposits

- Reduced management complexity of dealing with fewer institutions

- Enhanced negotiating power with a single larger deposit

- Simplified tax reporting with fewer T5 slips

For example, investing $100,000 at one institution might earn you 3.75%, while splitting $20,000 each across five institutions at their "best rate" of 3.50% would actually result in lower overall returns despite the effort of managing multiple accounts.

Negotiation leverage points

Understanding tier thresholds provides powerful negotiation leverage, even when you're slightly below the threshold amount:

- Near-threshold negotiation: If you're close to a threshold (e.g., $23,000 when the next tier is $25,000), ask if the institution will extend the higher tier rate.

- Relationship value: Highlight your overall relationship with the institution, including other accounts and services.

- Future deposits: Mention potential additional deposits or investments you may make.

- Competitor awareness: Show that you're aware of tier structures at competing institutions.

Pro Tip: When negotiating, always speak with someone who has rate authority, typically a branch manager or investment specialist, rather than a frontline teller.

Common GIC questions answered

Are GICs a good investment in 2026?

GICs remain a solid investment option for specific financial goals and situations in 2026. They're particularly valuable for:

- Capital preservation: When protecting your principal is the primary concern

- Known future expenses: When you need a specific amount at a predetermined time

- Risk balancing: As the stable component of a diversified portfolio

- Income generation: For predictable interest payments

The current interest rate environment makes GICs more attractive than they were during the ultra-low rate period of the early 2020s. Still, their primary value remains in security rather than growth.

How are GICs taxed in Canada?

The taxation of GIC interest depends on how your GIC is registered:

- TFSA GICs: Interest is completely tax-free

- RRSP/RRIF GICs: Interest grows tax-deferred until withdrawal, then taxed as income

- RESP GICs: Interest grows tax-deferred until withdrawal for education, then taxed as income for the student (typically at a lower rate)

- Non-registered GICs: Interest is fully taxable in the year it's earned (or deemed to be earned) at your marginal tax rate

For non-registered GICs, financial institutions issue T5 tax slips reporting the interest income you must declare on your tax return.

By the way — if high-interest debt is eating more than your GICs earn after tax, it may be worth prioritizing debt consolidation before going heavy on non-registered GICs. Lotly helps homeowners consolidate expensive debt using home equity, factoring in income sources that banks often ignore.

Can I cash out a GIC before maturity?

This depends on the type of GIC you purchase:

- Non-redeemable GICs: Generally cannot be cashed out before maturity except in rare hardship cases, and often with significant penalties

- Cashable/redeemable GICs: Can be cashed out after a minimum holding period (typically 30-90 days), usually with a reduced interest rate

- Market-linked GICs: Redemption policies vary by institution, but most cannot be redeemed early

If liquidity is a concern, consider:

- Using a GIC ladder for regular access to funds

- Choosing cashable GICs despite their lower rates

- Keeping a portion of your savings in high-interest savings accounts

What happens when my GIC matures?

When your GIC reaches its maturity date, you typically have several options:

- Automatic renewal: Many GICs automatically renew for the same term at the current rate unless you provide other instructions

- Reinvestment: Choose a new GIC term or product

- Transfer to another account: Move the funds to your checking or savings account

- Cash out: Receive the principal and interest as cash

Most financial institutions provide a "grace period" after maturity (typically 10-30 days) during which you can make these decisions without penalty.

Are GICs safe if a bank fails?

GICs are among the safest investments available in Canada due to deposit insurance protection:

- CDIC-member institutions: Since April 30, 2020, term deposits/GICs with terms greater than five years can be eligible for CDIC coverage (subject to other eligibility rules and CDIC membership).

- Credit unions: Provincial deposit insurance often provides even higher coverage (unlimited in some provinces)

To maximize protection for larger investments:

- Spread investments across different financial institutions

- Use different registration types (personal, joint, TFSA, RRSP, etc.)

- Consider credit unions with higher provincial coverage limits

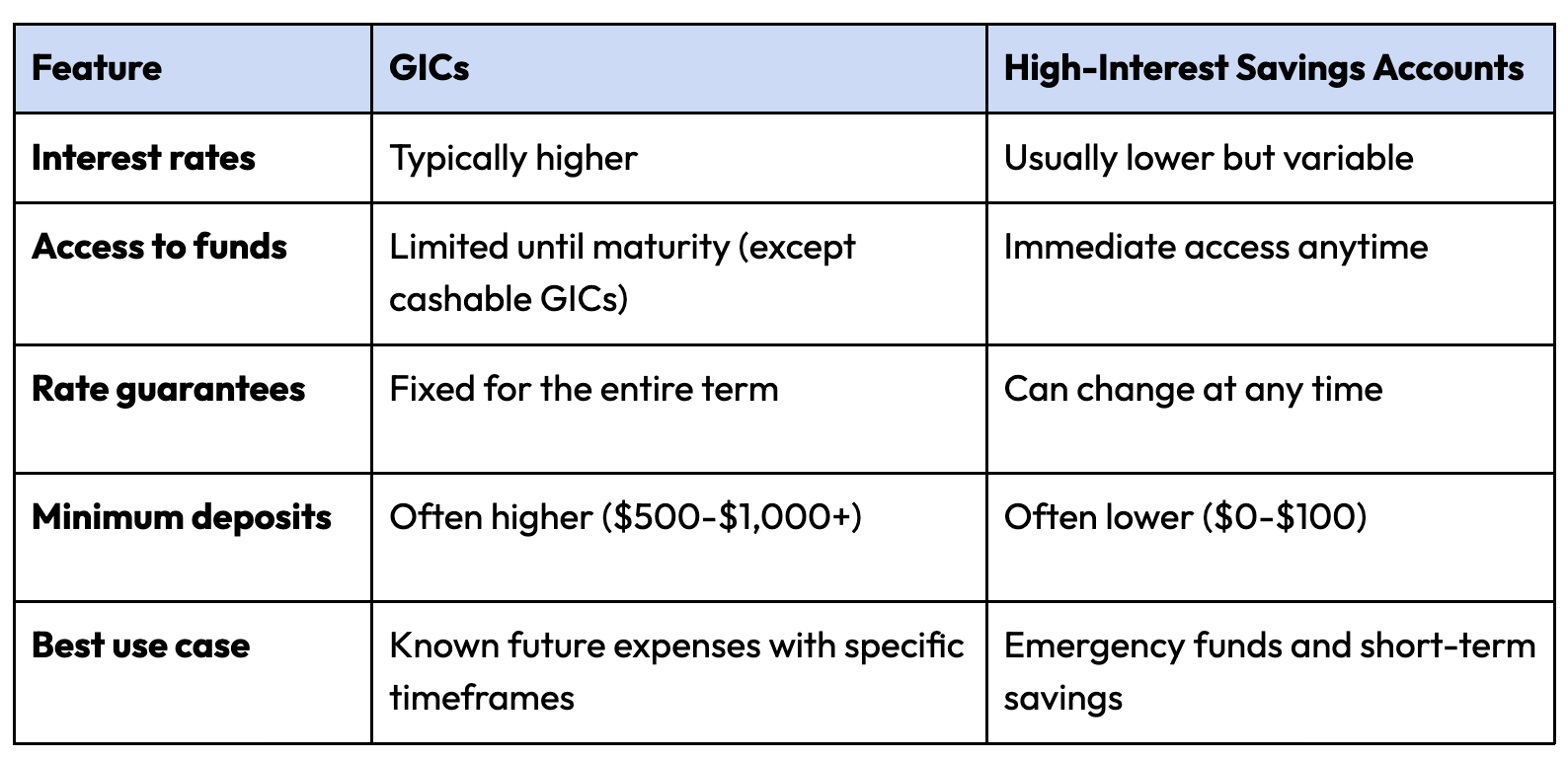

How do GICs compare to high-interest savings accounts?

Both GICs and high-interest savings accounts (HISAs) are secure savings vehicles, but they serve different purposes:

Many financial experts recommend using both: HISAs for emergency funds and immediate liquidity needs, and GICs for longer-term savings with specific time horizons.

Alternative approaches to fixed income investing

While GICs offer security and guaranteed returns, some investors may need higher yields or different features to meet their financial goals.

For investors seeking alternatives to standard GICs, consider:

- High-yield bonds: Potentially higher returns with increased risk

- Dividend stocks: Combine income with growth potential

- Real Estate Investment Trusts (REITs): Property-based income

- Preferred shares: Higher yields than GICs with some price volatility

- Bond ETFs: Diversified fixed-income exposure with liquidity

Each alternative comes with different risk profiles and features that may complement a GIC portfolio.

Ready to make your GICs work harder? Lotly can help

Securing the best GIC rates is just one part of a comprehensive financial strategy. Savvy investors know that balancing guaranteed returns with other opportunities creates the strongest foundation for long-term economic success.

Key takeaways:

- Understand GIC rate tiers to maximize your returns by strategically investing amounts that reach critical thresholds, potentially earning hundreds more in interest.

- Implement a GIC ladder strategy to balance liquidity needs with higher returns, ensuring you always have funds maturing while maintaining exposure to longer-term rates.

- Consider registered accounts first for your GIC investments, particularly TFSAs, to shield your interest earnings from taxation and maximize your after-tax returns.

- Look beyond the big banks for your GIC investments, as online banks and credit unions typically offer significantly higher rates that can substantially increase your returns over time.

P.S. If you're a homeowner looking to balance secure GIC investments with more flexible financial options, Lotly makes it simple. One form, real solutions, and a team that's on your side. Book a free consultation to see how you can leverage your home equity while maintaining your GIC investment strategy today.

Ayaz Virani

Ayaz Virani is the Vice President of Sales at Lotly and a licensed mortgage agent in Ontario under 8Twelve Mortgage Corporation (FSRA License #13072). With over three years of experience as a Growth Manager at KOHO Financial, Ayaz brings deep expertise in helping Canadians access smart, flexible financing. He has successfully funded hundreds of homeowners and is known for his transparent advice, fast service, and genuine care for each customer’s financial goals.