Summary

- HELOCs are secured by your home, making it easier to qualify for lower interest rates and higher loan amounts, even with imperfect credit.

- Unlike personal loans, HELOCs allow you to borrow, repay, and borrow again, making them ideal for ongoing and unexpected expenses.

- With a HELOC, you can access a larger sum of money (up to 65% of your home’s value) compared to personal loans.

Borrowing money is a necessity for many Canadians, whether it’s to renovate a home, consolidate debt, or cover unexpected expenses. Two popular options are personal loans and home equity lines of credit (HELOCs). While both can provide access to funds, they differ significantly in structure, cost, and flexibility.

Let's explore both financing options and find out why a HELOC might be the smarter choice for many homeowners.

What Is A Personal Loan?

A personal loan is a common form of borrowing and involves borrowing a lump sum of money that's repaid in regular installments over a set term. These are typically unsecured, which means you don’t need collateral.

You can get a personal loan from banks and other financial institutions, though larger amounts at low interest rates usually require strong credit and finances. That said, private lenders are a flexible alternative for those with limited or no credit.

Personal Loan Features

- Loan Amounts: $500 to $35,000+

- Loan Terms: 6 months - 5 years+

- Interest Rates: 9.99% - 35% (APR)

- Repayment Term: Regular installments (typically monthly)

What Is A HELOC?

A home equity line of credit (HELOC) allows you to borrow against the equity in your home. It's a type of revolving credit that allows you to borrow, repay, and borrow again up to your limit.

Since a HELOC is secured by your home, lenders typically offer lower interest rates compared to unsecured personal loans. Funds can be used for various purposes, including renovations, debt consolidation, or emergencies. HELOCs are attractive because they provide ongoing access to funds, much like a credit card.

HELOC Features

Loan Amounts: Up to 65% of your home's appraised value

Loan Terms: Revolving credit

Interest Rates:

- Variable rates - Tend to fluctuate with the lender's prime rate

- Typically lower than personal loan rates

Repayment Terms: Typically involve a draw period (interest-only payments) & repayment period (principal & interest)

What’s Better: A HELOC or A Personal Loan?

HELOCs and personal loans each come with unique advantages and potential downsides, so the better option ultimately depends on your financial needs and goals.

Pros Of A HELOC Over A Personal Loan

- Lower Rates: Because a HELOC is secured by your home, lenders typically offer lower interest rates than unsecured personal loans.

- Flexibility In Borrowing: You can draw funds as needed rather than taking a lump sum all at once.

- Interest-Only Payments: Many HELOCs allow you to pay just the interest during the draw period, which can alleviate pressure on short-term cash flow.

- Long-Term Access To Funds: A HELOC stays open for years, giving you ongoing access without having to reapply for new credit.

- May Be Easier To Qualify: HELOCs can be easier to access than personal loans because they’re secured by your home. This security often makes it easier to qualify for, even if your credit isn’t perfect.

- Larger Loans: Depending on the equity in your home, you can borrow large sums of money, which can help cover major expenses like renovations or repairs. For example, if your home is worth $600,000 and you still owe $250,000 on your mortgage, you could borrow up to $140,000.

Cons Of A HELOC Over A Personal Loan

A HELOC can come with certain drawbacks to consider:

- Home Is At Risk: Since the loan is secured by your home, staying on top of payments is important, as missed payments can put your home at risk.

- Variable Interest Rates: HELOC rates often fluctuate, which means your payments can rise unexpectedly.

- Requires Discipline: It can be tempting to overspend thanks to a HELOC’s easy access to funds, which can make it harder to manage debt responsibly.

Pros Of A Personal Loan Over A HELOC

- Predictable Payments: Fixed interest rates and repayment schedules make budgeting straightforward.

- No Collateral Required: Loan approval is based on creditworthiness, so your home isn’t tied to the loan and at risk of seizure if you don’t repay.

Cons Of A Personal Loan Over A HELOC

- Higher Interest Rates: Unsecured loans usually come with higher rates compared to home equity loans, which are secured.

- Limited Flexibility: You receive a lump sum upfront and must reapply to borrow more.

- Shorter Terms: Repayment periods are typically shorter, which can mean higher monthly payments.

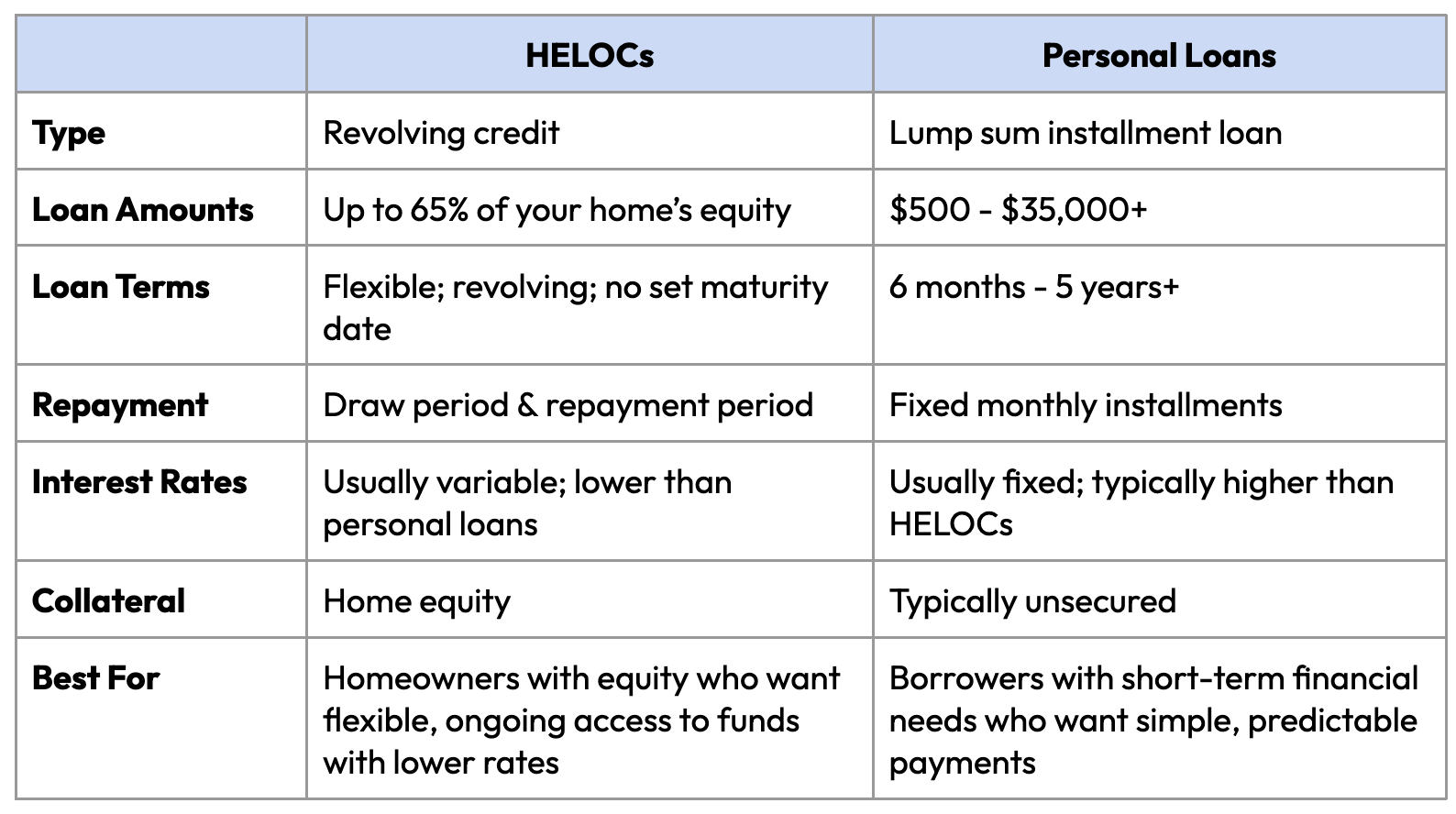

HELOC Vs Personal Loan: How Do They Compare?

The following chart provides a clear comparison of the most important features of HELOCs and personal loans:

When Should You Choose A HELOC?

HELOCs make most sense in several scenarios, like the following:

- Home Renovations. Ideal for funding ongoing renovation projects where costs may vary over time.

- Debt Consolidation. If you have a lot of high-interest-rate loans like credit cards and payday loans, a HELOC can help you consolidate at a lower rate, helping you save money and lower your monthly payments.

- You Have Bad Credit. A HELOC can be a great option if your credit isn’t perfect, since many lenders are willing to approve borrowers when the loan is secured by your home.

- Emergency Fund Access. If you want a financial cushion for unexpected expenses, a line of credit allows you to have immediate access to funds without needing to reapply for a loan.

When Should You Choose A Personal Loan?

There may be cases where a personal loan might be more useful than a HELOC:

- One-Time Expenses. Best for covering a single, specific cost such as a wedding, car repair, or medical bill.

- No Home Equity. If you don’t own a home and have no home equity, an unsecured personal loan is the obvious choice over a HELOC.

- Predictable Repayment. Works well if you prefer fixed monthly payments and a clear timeline for repayment.

Why Might A HELOC Be The Smarter Choice Over A Personal Loan?

A HELOC can be a smarter choice than a personal loan because it typically offers lower interest rates, since it’s secured by your home. Unlike a personal loan’s lump sum, a HELOC provides flexible, revolving access to funds, making it ideal for ongoing or unpredictable expenses, like renovations or tuition.

Many HELOCs also allow interest-only payments during the draw period, easing short-term cash flow. For homeowners with equity, this combination of lower costs and long-term access often makes a HELOC more versatile than a personal loan.

Final Thoughts

In the end, a HELOC often stands out as the smarter choice because it combines lower borrowing costs with the flexibility to access funds whenever you need them. While personal loans offer predictability, a HELOC’s revolving credit and long-term availability make it especially useful for homeowners managing variable expenses.

If you’re looking to secure a HELOC that fits your needs, Lotly is a great place to start. They help Canadian homeowners access clear, competitive home equity options. They review your full financial picture and guide you to the solution that works best for you. Book a free consultation to get started.

If you don’t have equity or simply want to explore other borrowing options, Loans Canada can help. You can explore different loan options, compare rates, check your credit score, and access helpful tools and resources to support your research.

FAQs

What is the main difference between a HELOC and a personal loan?

A personal loan provides a lump sum with fixed payments, while a HELOC offers revolving credit secured by your home.

Why might a HELOC be considered the smarter choice?

A HELOC often comes with lower interest rates and offers flexible borrowing, making it useful for ongoing or variable expenses.

Can you use a HELOC to purchase a car?

Yes, you can use a HELOC to buy a car in Canada. Although it’s more common to use a car loan for this type of purchase, a HELOC is still something to consider if you own a home and have significant equity.

Which option has lower interest rates?

HELOCs typically come with lower rates than a personal loan because they’re backed by your home’s equity.

How much can you borrow using a HELOC?

You can generally borrow up to 65% of your home value. This means if your home is worth $600,000 and you still owe $250,000 on your mortgage, you could borrow up to $140,000.

Ayaz Virani

Ayaz Virani is the Vice President of Sales at Lotly and a licensed mortgage agent in Ontario under 8Twelve Mortgage Corporation (FSRA License #13072). With over three years of experience as a Growth Manager at KOHO Financial, Ayaz brings deep expertise in helping Canadians access smart, flexible financing. He has successfully funded hundreds of homeowners and is known for his transparent advice, fast service, and genuine care for each customer’s financial goals.