Summary

- Preparation matters. Take time to address minor repairs, organize documentation, and present your home at its best before an appraisal.

- Focus on what you can control. While you can't change your home's location or broader market conditions, you can highlight improvements and ensure the appraiser has complete information.

- Know your options. If an appraisal comes in lower than expected, understand the steps for requesting reconsideration or exploring alternative financing solutions.

- Think strategically about equity. Use your home's appraised value to make informed decisions about accessing equity for debt consolidation, home improvements, or other financial needs.

How much is your home really worth? It’s not what you paid. It’s not what your neighbour thinks. And it’s not what your city says on your tax bill. In Canada, your home’s true market value comes down to one thing: a professional appraisal.

(Plus, of course, whatever someone’s willing to pay for it!) Whether you’re applying for a mortgage, tapping into your equity, or just trying to set a smart selling price, your home appraisal can make or break the deal—and your financing.

In this complete guide, you’ll learn:

- What a home appraisal is (and how it’s different from a home inspection or tax assessment)

- When and why you’ll need one—mortgages, HELOCs, refinances, and more

- Exactly how appraisers determine your home’s value (and what factors matter most)

- What to do before, during, and after the appraisal to get the best result

- How the final number impacts your borrowing power, interest rates, and equity

- What to do if the appraisal comes in too low—and how to challenge it the right way

Ready? Let’s go!

By the way — Looking to unlock your home’s equity? Lotly makes home equity financing simple and stress-free, helping Canadian homeowners leverage their property’s value—regardless of traditional credit challenges. Find out how much equity you can comfortably access today.

What is a home property appraisal?

A home property appraisal is an unbiased estimate of your property's fair market value conducted by a licensed, third-party professional. Unlike the price you might set when selling your home or the assessed value used for property taxes, an appraisal represents what your property is objectively worth in the current real estate market.

- Appraisals serve as a safeguard in real estate transactions, ensuring that the amount being financed through a mortgage or home equity loan is appropriate for the property's actual value.

- They protect both lenders and borrowers by confirming that the property can serve as adequate collateral for the loan amount.

In Canada, professional appraisers follow standardized methods and adhere to strict guidelines established by organizations like the Appraisal Institute of Canada (AIC) to determine your home's value.

When is a home appraisal required in Canada?

Home appraisals aren't necessary for every property-related decision, but several common situations typically trigger the need for a professional valuation. Understanding when an appraisal is required can help you prepare both financially and logistically.

Mortgage applications and refinancing

When you apply for a new mortgage or refinance an existing one, your lender will almost always require an appraisal. This is because the property serves as collateral for the loan, and lenders need to verify that its value supports the loan amount.

For refinancing, even if you've been with the same lender for years, an updated appraisal is typically required since property values can change significantly over time. The appraisal helps determine your current loan-to-value ratio, which impacts your refinancing options and interest rates.

Home equity loans and lines of credit

Accessing your home's equity through a home equity loan or line of credit also requires an appraisal. These financial products allow you to borrow against the equity you've built in your home – the difference between your home's current market value and your outstanding mortgage balance.

The appraisal determines how much equity you can access, as most lenders in Canada will allow you to borrow up to 80% of your home's appraised value, minus your existing mortgage balance. For homeowners with diverse financial backgrounds, including those with credit challenges, the appraisal becomes especially important as it focuses on the property's value rather than just credit history.

Property sales and purchases

While not always required by law, appraisals are common in property transactions. Buyers may request an appraisal to ensure they're not overpaying, while sellers might get an appraisal to help set an appropriate asking price.

If the buyer is financing the purchase, their lender will require an appraisal as part of the mortgage approval process. This typically happens after an offer is accepted but before the mortgage is finalized, usually within 5 to 10 business days.

Can you skip the appraisal?

Depending on the lender and the type of loan you’re considering, you might be eligible for an Automated Valuation Model (AVM) instead of a traditional in-person appraisal:

- An AVM uses advanced data analytics to quickly estimate your home’s value, streamlining the loan approval process.

- Keep in mind that not all lenders or property types qualify for AVMs.

Lenders or mortgage brokers may use an AVM initially to screen or pre-qualify a deal before ordering a full appraisal. AVMs can replace the appraisal in specific situations, but their acceptance depends on the lender, insurer, loan type, and risk profile.

The home appraisal process in Canada

Understanding what happens during a home appraisal can help reduce anxiety and ensure you're prepared when the appraiser arrives. The process follows a structured approach designed to provide an objective evaluation of your property.

Who conducts home appraisals?

In Canada, home appraisals are conducted by licensed professionals who have completed extensive education and training. Most appraisers hold designations from the Appraisal Institute of Canada (AIC), such as:

- Canadian Residential Appraiser (CRA®): Qualified to appraise single-family homes, semi-detached houses, townhouses with up to four units, condominiums, and residential vacant land.

- Accredited Appraiser Canadian Institute (AACI®): Qualified to appraise a wider range of properties, including land, agricultural properties, commercial, and residential buildings.

These designations require rigorous education, practical experience (often 1-3 years working under a mentor), and passing professional examinations. When selecting an appraiser, look for these credentials along with professional liability insurance and strong local market knowledge.

What happens during the appraisal visit?

The on-site inspection is a crucial part of the appraisal process. Here's what typically occurs:

- Property inspection: The appraiser examines both the interior and exterior of your home, typically spending 1-2 hours on site.

- Documentation: They take measurements, photographs, and notes about your property's features, condition, and any recent renovations or upgrades.

- Assessment of features: The appraiser evaluates key elements like the number of bedrooms and bathrooms, square footage, layout, and overall condition of the property.

- Neighborhood analysis: They also consider the surrounding area, including proximity to amenities, schools, and other factors that influence property values.

During this visit, you can provide information about recent improvements, unique features, or other aspects that might positively impact your home's value.

How appraisers determine your home's value

After the physical inspection, appraisers use several methods to calculate your home's value:

- Comparable sales approach: The most common method for residential properties involves analyzing at least three recently sold comparable properties ("comps") in your neighborhood. The appraiser adjusts for differences between your home and these comparables.

- Cost approach: This estimates what it would cost to rebuild your home from scratch, plus the value of the land, minus depreciation.

- Income approach: Primarily used for investment properties, this method evaluates the potential rental income the property could generate.

The final appraisal report, often 10-15 pages or more, includes detailed descriptions, photographs, market analysis, and the final valuation. This report typically takes several days to complete after the site visit and is then provided to the lender who ordered the appraisal.

Key factors that affect your home's appraisal value

Multiple elements influence your home's appraised value. Understanding these factors can help you maximize your property's worth before an appraisal.

Location and neighborhood factors

Location remains one of the most significant determinants of property value. Appraisers consider:

- Proximity to amenities: Access to shopping centers, restaurants, parks, and public transportation

- School district quality: Highly-rated schools typically boost property values

- Neighborhood desirability: Safety, appearance, and development of the surrounding area

- Market trends: Whether property values in your area are rising, stable, or declining

A home in a desirable neighborhood with strong amenities will generally appraise higher than a similar property in a less sought-after location.

Property size, features, and condition

Physical characteristics of your property play a crucial role in its appraised value:

- Square footage: Larger homes typically appraise for more, though the value per square foot may decrease as size increases

- Number of bedrooms and bathrooms: More rooms generally increase value, particularly in family-oriented neighborhoods

- Layout and functionality: Practical, flowing floor plans are valued higher than awkward layouts

- Overall condition: Well-maintained homes with updated systems (electrical, plumbing, HVAC) command higher values

- Age of the property: Newer homes often appraise higher, though historical properties can be valuable in certain markets

Appraisers look beyond cosmetic features to assess the fundamental condition and functionality of your home.

Renovations and improvements

Not all home improvements deliver equal returns on investment when it comes to appraisal value.

Renovations that tend to increase value include:

- Kitchen updates: Modern appliances, countertops, and cabinets

- Bathroom renovations: Updated fixtures, tile work, and layouts

- Finished basements: Adding usable living space

- Energy-efficient upgrades: New windows, doors, and improved insulation

- Roof replacement: Especially if the current roof is aging or damaged

Improvements that may not significantly impact appraisal value include:

- Swimming pools: Especially in neighborhoods where they're uncommon

- Luxury upgrades: High-end finishes that exceed neighborhood standards

- Highly personalized spaces: Converted rooms with very specific purposes

- Extensive landscaping: While curb appeal matters, elaborate gardens may not add proportional value

To maximize return on investment, focus on improvements that enhance functionality and appeal while remaining consistent with neighborhood standards.

Current market conditions

The broader real estate market significantly influences appraisal values:

- Supply and demand: Limited inventory in a high-demand market drives values up

- Interest rates: Lower rates typically increase buying power and property values

- Economic factors: Local employment rates, business growth, and overall economic health

- Seasonal fluctuations: In some markets, values vary depending on the time of year

Appraisers consider these market dynamics when determining your home's current value, which is why the same property might appraise differently just months apart.

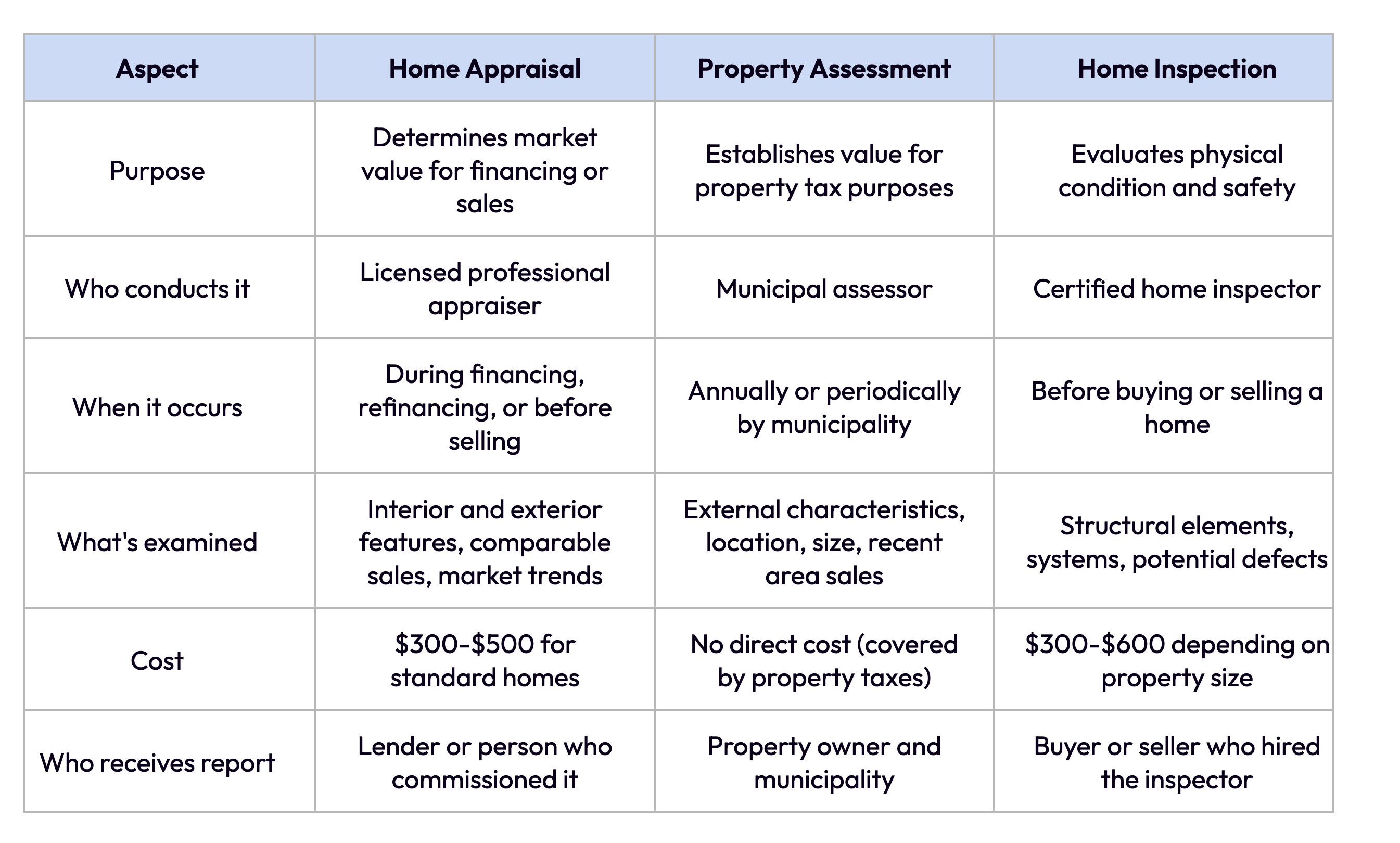

Home appraisal vs. Property assessment vs. Home inspection

These three property evaluations serve different purposes and are conducted by different professionals. Understanding the distinctions can help you avoid confusion during real estate transactions.

While all three evaluations involve your property, they serve distinct purposes and shouldn't be confused or used interchangeably.

Cost of home appraisals in Canada

The cost of a home appraisal in Canada varies based on several factors, including property type, location, and complexity. Understanding these costs helps you budget appropriately when an appraisal is needed.

Standard residential appraisals

For typical single-family homes, townhouses, and condominiums, appraisal costs generally range from:

- Urban areas: $350-$500

- Rural areas: $300-$450

Factors affecting appraisal costs

Several elements can increase the standard appraisal fee:

- Property size and complexity: Larger homes or those with unique features require more time and expertise

- Location: Remote properties may incur travel charges

- Urgency: Rush orders typically cost 25-50% more than standard timelines

- Property type: Multi-unit buildings or properties with mixed uses cost more to appraise

- Purpose: Some specialized appraisals (like those for legal proceedings) require additional documentation

Who pays for the appraisal?

In most cases, the party requesting the loan (the borrower) pays for the appraisal. However, some lenders may cover the cost as part of their mortgage package, especially for refinancing. When you're applying for a home equity loan or line of credit, you'll typically pay the appraisal fee upfront or have it included in your closing costs.

How to prepare for a home appraisal

Taking the right steps before an appraiser visits can help ensure your property shows its best value. While you can't change factors like location or market conditions, you can optimize what's within your control.

Before the appraiser arrives

Preparation in the days or weeks before an appraisal can make a significant difference:

- Address minor repairs: Fix leaky faucets, replace broken light fixtures, repair holes in walls, and touch up paint

- Enhance curb appeal: Mow the lawn, trim bushes, clear walkways, and ensure the exterior looks well-maintained

- Clean thoroughly: A clean home suggests good maintenance and care

- Declutter: Remove excess items to make spaces appear larger and more functional

- Complete unfinished projects: Finish any half-done renovations that might detract from your home's appearance

These improvements won't dramatically change your home's value, but they help create a positive impression and ensure the appraiser sees your property at its best.

During the appraisal

When the appraiser visits, these actions can facilitate an effective evaluation:

- Be present but not intrusive: Make yourself available for questions without following the appraiser around

- Provide access to all areas: Ensure the appraiser can easily inspect every part of your property

- Point out improvements: Mention significant upgrades or renovations, especially those not immediately visible

- Share neighborhood insights: Information about recent improvements to the area or upcoming developments may be relevant

- Be honest: Don't attempt to hide problems or exaggerate features

Remember that appraisers are professionals looking for objective information, not trying to find faults in your home.

Documentation to have ready

Prepare these documents to support your home's valuation:

- List of improvements: Compile dates and costs of significant renovations, updates, or additions

- Permits and approvals: Have copies of permits for any major work completed

- Floor plan: If available, provide a current floor plan showing the layout and dimensions

- Recent comparable sales: If you're aware of similar homes that have sold for good prices, note these for the appraiser

- Details of unique features: Document any energy-efficient systems, smart home technology, or other special features

Providing this information upfront helps ensure the appraiser has all relevant facts when determining your home's value.

What to do if you disagree with your home appraisal

Receiving a lower-than-expected appraisal can be disappointing, especially when it affects your financing options. However, you have several potential courses of action.

Review the appraisal report

Start by carefully examining the appraisal report for any errors or omissions:

- Property details: Check that square footage, room counts, and features are accurate

- Comparable properties: Assess whether the selected comps truly reflect your home's characteristics

- Recent improvements: Verify that significant renovations or upgrades were noted

- Neighborhood factors: Ensure that positive aspects of your location were considered

Identifying specific issues provides a foundation for challenging the appraisal if necessary.

Request a Reconsideration of Value (ROV)

If you find clear errors or omissions, you can request a Reconsideration of Value through your lender:

- Document the issues: Compile evidence of inaccuracies or overlooked features

- Suggest better comparables: If you know of more appropriate recent sales, provide these details

- Submit supporting materials: Include photos, receipts for improvements, and other relevant documentation

- Work through your lender: Submit your request to the lender who ordered the appraisal, not directly to the appraiser

Keep your request factual and specific, focusing on objective information rather than emotional appeals.

Consider a second appraisal

In some cases, getting a second opinion may be worthwhile:

- Discuss with your lender: Some lenders will consider a second appraisal if there are legitimate concerns

- Be prepared to pay: You'll typically need to cover the cost of any additional appraisal

- Use a different appraiser: Ensure the second appraiser has strong knowledge of your local market

- Understand the limitations: The lender may still use the lower of the two appraisals

A second appraisal is most effective when the first contained clear errors or when the appraiser lacked familiarity with your neighborhood.

Explore alternative financing options

If challenging the appraisal doesn't yield results, consider these alternatives:

- Negotiate with the seller: If you're buying, ask the seller to lower the price to match the appraisal

- Increase your down payment: Adding more cash can bridge the gap between the appraised value and purchase price

- Explore different lenders: Some lenders offer more flexible approaches to property valuation

- Consider alternative financing: Options like private loans or seller financing might be available

- Wait and reapply: In a rising market, waiting a few months might result in a higher appraisal

For homeowners seeking to access equity despite a lower-than-expected appraisal, working with lenders who focus on the property's value rather than just credit history can provide additional options.

How home appraisals impact your home equity financing options

The appraised value of your home directly affects your ability to access its equity through loans or lines of credit. Understanding this relationship helps you make informed financing decisions.

Calculating available equity

Lenders typically use this formula to determine how much equity you can access:

- Calculate 80% of your home's appraised value (the maximum loan-to-value ratio most lenders allow)

- Subtract your current mortgage balance

- The remaining amount represents your accessible equity

For example, if your home appraises for $500,000 and you owe $300,000 on your mortgage:

- 80% of $500,000 = $400,000

- $400,000 - $300,000 = $100,000 in accessible equity

This means you could potentially borrow up to $100,000 through a home equity loan or line of credit.

Impact of appraisal value on financing terms

Beyond determining how much you can borrow, your home's appraised value affects other aspects of equity financing:

- Interest rates: Higher loan-to-value ratios typically result in higher interest rates

- Approval odds: Stronger equity positions improve your chances of approval, even with credit challenges

- Loan options: More equity gives you access to a wider range of financing products

- Closing costs: Some costs are calculated as a percentage of the loan amount, which is based on your equity

For homeowners with diverse financial backgrounds, including those with credit challenges or non-traditional income, the appraisal becomes especially important as it focuses on the property's value rather than just credit history.

Maximizing your equity position

To improve your financing options through home equity:

- Time your application strategically: If possible, apply when market values are strong

- Complete high-value improvements before appraisal: Focus on renovations with strong returns on investment

- Reduce your existing mortgage: Paying down your current mortgage increases available equity

- Work with equity-focused lenders: Some lenders specialize in home equity solutions and may offer more flexible terms

By understanding how appraisals impact your financing options, you can make strategic decisions about when and how to access your home's equity.

The equity access readiness checklist

Before applying for home equity financing, use this checklist to ensure you're positioned to maximize your property's appraised value and streamline the process.

Property documentation readiness

Organize these documents to support your home's valuation:

- Home improvement records: Compile receipts, contracts, and before/after photos of significant renovations

- Maintenance documentation: Gather records of major system replacements (roof, HVAC, etc.)

- Permit history: Collect permits and approvals for any structural changes or additions

- Warranty information: Assemble warranties for newer appliances, systems, or features

- Previous appraisal reports: If available, have recent appraisals ready for reference

Having this documentation organized demonstrates your home's value and helps the appraiser understand its history and improvements.

Pre-appraisal property enhancement guide

Complete these high-impact, low-cost improvements 1-4 weeks before your appraisal:

- Exterior touch-ups: Paint the front door, clean siding, repair visible cracks

- Landscaping refresh: Trim overgrown plants, add fresh mulch, remove dead vegetation

- Interior maintenance: Fix leaky faucets, squeaky doors, and other minor issues

- Deep cleaning: Professional carpet cleaning, window washing, and general thorough cleaning

- Decluttering: Remove excess furniture and personal items to make spaces appear larger

These targeted improvements create a positive impression without requiring major investments.

Comparable property analysis template

Research similar properties in your neighborhood that have recently sold:

Appraisal day preparation timeline

Follow this countdown to ensure everything is ready:

One week before:

- Complete all minor repairs

- Schedule professional cleaning if needed

- Organize documentation

Three days before:

- Confirm appraiser appointment time

- Begin thorough cleaning

- Identify and address any overlooked maintenance issues

One day before:

- Mow lawn and complete final landscaping touch-ups

- Clean all windows and mirrors

- Ensure all lights work and replace any burnt-out bulbs

- Remove pets and their supplies temporarily if possible

Day of appraisal:

- Open curtains and blinds to maximize natural light

- Turn on all lights

- Ensure comfortable temperature

- Have documentation readily available

- Secure pets away from the appraiser's path

This systematic approach helps ensure your property presents its best value during the critical appraisal visit.

Unlock the power of you home’s value today with Lotly

Understanding the home appraisal process empowers you to make strategic decisions about your property and its equity. With proper preparation and knowledge, you can approach appraisals with confidence rather than anxiety.

Remember these key takeaways:

- Preparation matters. Take time to address minor repairs, organize documentation, and present your home at its best before an appraisal.

- Focus on what you can control. While you can't change your home's location or broader market conditions, you can highlight improvements and ensure the appraiser has complete information.

- Know your options. If an appraisal comes in lower than expected, understand the steps for requesting reconsideration or exploring alternative financing solutions.

- Think strategically about equity. Use your home's appraised value to make informed decisions about accessing equity for debt consolidation, home improvements, or other financial needs.

Whether you're buying, selling, refinancing, or accessing your home's equity, a thorough understanding of the appraisal process helps ensure you receive fair value for your most important asset.

Wondering how much equity you might be able to access in your home? Lotly offers free, no-obligation consultations to help you understand your options, regardless of your credit history or income type. Our team specializes in finding flexible solutions for Canadian homeowners looking to leverage their property's value for debt consolidation, home improvements, or other financial needs.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.