Summary

- Consumer proposals offer significant debt reduction and legal protection while allowing you to keep your assets, but they impact your credit for several years.

- Home equity debt consolidation preserves your credit standing and may offer lower interest rates, but it requires sufficient equity and income qualification.

- The best solution depends on your unique situation, including your debt level, income stability, equity position, and future financial goals.

- Professional guidance from Licensed Insolvency Trustees, financial advisors, or home financing specialists can help you make an informed decision.

Drowning in debt but afraid of losing your home? You’re not alone, and you do have options. For Canadian homeowners struggling with credit cards, tax bills, or other unsecured debt, the fear of falling behind can feel overwhelming. But contrary to what many think, insolvency doesn’t always mean bankruptcy — or giving up your house.

A consumer proposal offers a powerful middle ground. In this step-by-step guide, you’ll learn:

- Exactly how consumer proposals work (and how they differ from bankruptcy)

- Whether you qualify and how to file with a Licensed Insolvency Trustee

- What to expect during the process — including how it impacts your credit

- Alternatives like home equity debt consolidation (and when they make more sense)

- How to weigh your options and build a path toward financial recovery

If you’re a homeowner trying to break free from debt without losing everything you’ve built—this guide is for you.

By the way, are you looking for a better way to consolidate debt without insolvency? Lotly specializes in straightforward home equity consolidation loans, designed specifically to help Canadian homeowners manage high-interest debt responsibly — preserving your credit and keeping your home equity intact. Book a free consultation today to learn more.

What is a consumer proposal?

A consumer proposal is a legally binding debt settlement agreement between you and your creditors, administered under the Bankruptcy and Insolvency Act of Canada. Unlike debt management plans or informal settlements, a consumer proposal is a formal legal process that must be filed through a Licensed Insolvency Trustee (LIT).

The core benefit of a consumer proposal is that it allows you to settle your unsecured debts for less than the full amount owed, often reducing your debt by up to 70-80%. Once approved, you make fixed monthly payments (with no interest) for up to five years. During this time, you're legally protected from collection actions, wage garnishments, and lawsuits from creditors included in the proposal.

Consumer proposals have become increasingly common in Canada, now accounting for approximately 80% of all insolvency filings. This popularity stems from the fact that, unlike bankruptcy, you can keep your assets (including your home) while still obtaining significant debt relief.

For homeowners specifically, a consumer proposal can be an attractive option because it addresses unsecured debts without putting your home at risk, provided you continue making your mortgage payments.

How does a consumer proposal work in Canada?

A consumer proposal works by having a Licensed Insolvency Trustee negotiate with your creditors on your behalf. The trustee helps determine what you can reasonably afford to pay, then creates a formal offer to your creditors proposing to settle your debts for a percentage of what you owe.

The key mechanics include:

- Debt consolidation: All your unsecured debts are consolidated into one monthly payment.

- Interest elimination: Once filed, interest stops accumulating on the debts included in the proposal.

- Payment structure: You make one monthly payment to your trustee, who then distributes funds to your creditors.

- Legal protection: Filing grants immediate legal protection through a "stay of proceedings," stopping collection calls, lawsuits, and wage garnishments.

- Asset protection: Unlike bankruptcy, you keep all your assets, including your home, vehicle, and investments.

For example, suppose you owe $40,000 in credit card debt. In that case, a consumer proposal might reduce this to approximately $16,000 (40% of the original amount), paid over 60 months at about $267 per month with no interest.

The consumer proposal process: step-by-step

Understanding the timeline and process can help you prepare for what to expect when filing a consumer proposal:

- Initial consultation (1-2 hours): Meet with a Licensed Insolvency Trustee for a free assessment of your financial situation. The trustee will review your income, expenses, assets, and debts to determine if a consumer proposal is appropriate.

- Proposal development (1-2 weeks): If a consumer proposal is suitable, your trustee will work with you to develop a reasonable offer based on your ability to pay and what creditors are likely to accept.

- Filing the proposal (1 day): Once you agree on the terms, your trustee files the proposal with the Office of the Superintendent of Bankruptcy, triggering immediate legal protection from creditors.

- Creditor review period (45 days): Creditors have 45 days to vote on your proposal. If creditors holding more than 25% of your debt value request a meeting, one will be held. Otherwise, the proposal is deemed accepted.

- Approval and implementation: Once approved, you begin making your agreed-upon monthly payments to the trustee.

- Mandatory counseling (Two sessions): You must complete two financial counseling sessions during the proposal period.

- Completion and discharge (Up to 5 years): After making all required payments, you receive a "Certificate of Full Performance," officially releasing you from the debts included in the proposal.

The entire process, from filing to completion, typically takes 3-5 years, though you can pay off your proposal early if your financial situation improves.

Eligibility requirements for filing a consumer proposal

Not everyone qualifies for a consumer proposal. To be eligible, you must meet these requirements:

- Debt threshold: Your total unsecured debts must not exceed $250,000 (excluding your mortgage).

- Insolvency status: You must be insolvent, meaning you're unable to pay your debts as they become due, or the value of your assets is less than your liabilities.

- Residency: You must be a Canadian resident or own property in Canada.

- Income stability: You need sufficiently stable income to make the proposed monthly payments.

- Better than bankruptcy: The proposal must offer creditors more than they would receive if you filed for bankruptcy.

Note that only unsecured debts (like credit cards, unsecured lines of credit, payday loans, and tax debts) can be included in a consumer proposal. Secured debts like mortgages and car loans are not included, though you must continue paying these to keep the associated assets.

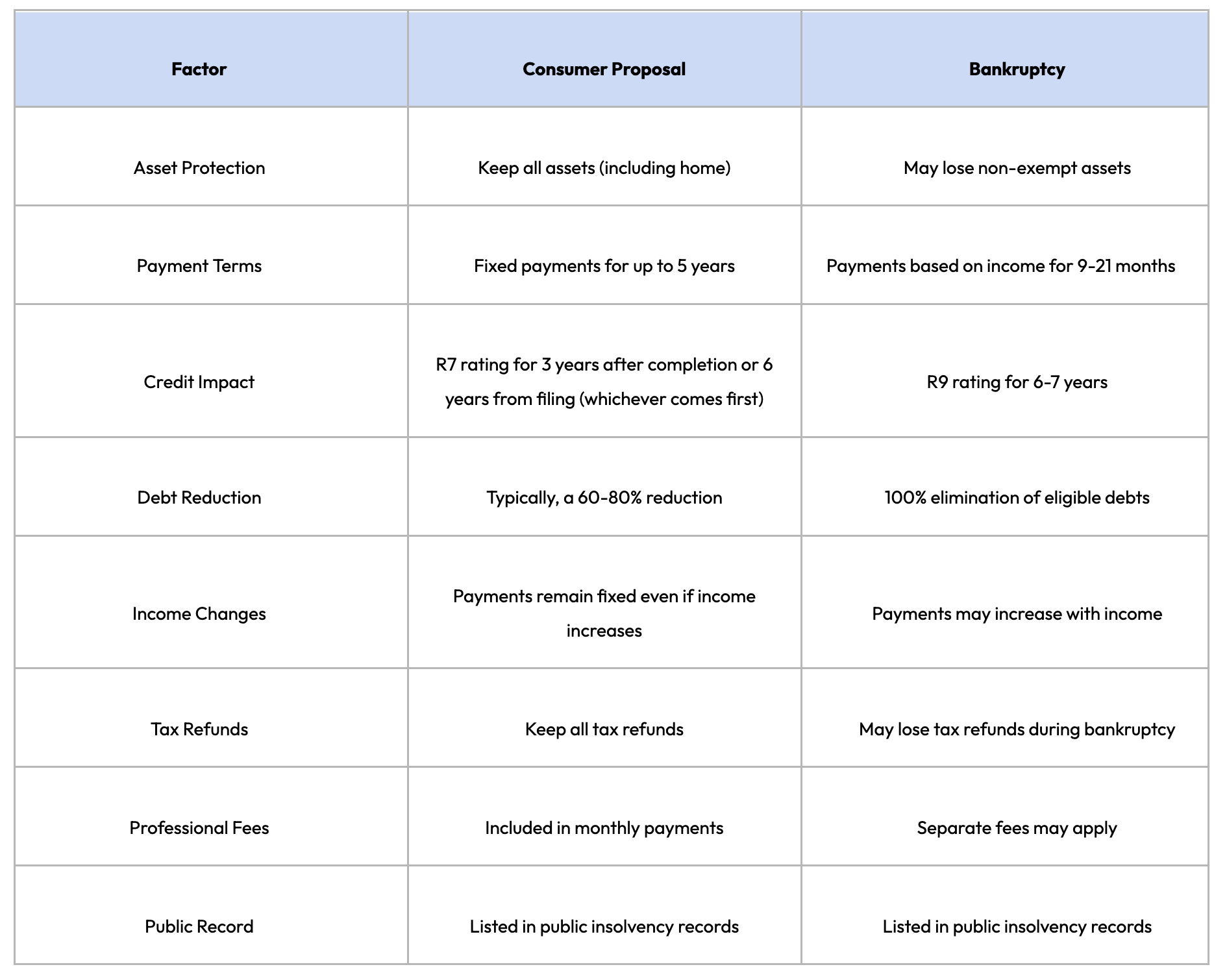

Consumer proposal vs. bankruptcy: which is right for you?

When considering debt relief options, many Canadians must decide between a consumer proposal and bankruptcy. Here's how they compare across key factors:

For homeowners, the asset protection aspect of a consumer proposal is particularly valuable. With bankruptcy, if you have significant equity in your home, you might be required to surrender some of that equity to your creditors. A consumer proposal allows you to keep your home and all accumulated equity, provided you maintain your mortgage payments.

Advantages and disadvantages of consumer proposals

Before deciding on a consumer proposal, it's crucial to understand both the benefits and drawbacks of this debt solution.

Benefits of filing a consumer proposal

- Significant debt reduction: Typically reduces unsecured debt by 60-80%, with no interest accumulating after filing.

- Asset protection: You keep all your assets, including your home, vehicle, and investments.

- Legal protection: Immediate stay of proceedings stops collection actions, wage garnishments, and lawsuits.

- Fixed payments: Unlike bankruptcy, payments don't increase if your income rises during the proposal period.

- Simplified debt management: Consolidates multiple debts into one affordable monthly payment.

- Less credit impact: While still significant, the impact on your credit is less severe and shorter-lasting than bankruptcy.

- Tax benefits: You keep all tax refunds, and there are no surplus income payments.

- Professional support: Receive guidance from a Licensed Insolvency Trustee throughout the process.

Drawbacks and limitations to consider

- Credit impact: Your credit report will display an R7 rating, which can make it challenging to obtain new credit during and shortly after the proposal.

- Time commitment: The process typically takes 3-5 years to complete.

- Public record: Consumer proposals are recorded in the public insolvency registry.

- Creditor approval required: Unlike bankruptcy, creditors must approve your proposal, and they may reject it if they feel the offer is too low.

- Not all debts included: Secured debts, student loans less than 7 years old, court fines, and child support cannot be included.

- Potential for default: If you miss three payments, your proposal may be deemed null and void, leaving you back where you started.

- Limited to $250,000: Unsecured debts cannot exceed $250,000 (excluding mortgage on principal residence).

How a consumer proposal affects your credit

One of the most significant concerns for many considering a consumer proposal is its impact on their credit. Understanding this impact can help you make an informed decision and plan for recovery.

When you file a consumer proposal, the credit bureaus (Equifax and TransUnion) are notified, and your credit report is updated with an R7 rating. This rating indicates that you've settled your debts for less than the full amount through a formal arrangement.

Here's what happens to your credit during and after a consumer proposal:

- During the proposal: While making payments, your credit rating will be R9 (the lowest possible rating).

- After completion: Once you have completed all payments, your rating will improve to R7.

- Removal timeline: The consumer proposal notation remains on your credit report for either 3 years after completion or 6 years from the filing date, whichever comes first.

- Credit score impact: Your credit score will likely drop significantly, often below 600, making it difficult to qualify for traditional loans and credit cards.

The good news is that you can begin rebuilding your credit immediately after filing. Some strategies include:

- Secured credit cards: Obtain a secured credit card by providing a security deposit.

- Credit builder loans: Consider products specifically designed to help rebuild credit.

- Timely payments: Ensure all payments (including those not in the proposal) are made on time.

- Credit utilization: Keep credit card balances below 30% of your limit.

- Early completion: Pay off your proposal early to start the credit recovery clock sooner.

With consistent effort, many people see significant credit improvement within 1-2 years after completing their consumer proposal, though full recovery typically takes 3-4 years.

Alternatives to consumer proposals

While consumer proposals offer significant benefits, they're not the only option for debt relief. Before making a decision, it's worth exploring alternatives that better suit your situation, especially if you're a homeowner with equity.

Debt consolidation through home equity

For homeowners with equity, leveraging that equity can be a powerful alternative to formal insolvency proceedings. Home equity debt consolidation works by using the value built up in your property to pay off high-interest unsecured debts.

Options include:

- Mortgage refinancing: Replace your existing mortgage with a new, larger one, using the additional funds to pay off other debts. This typically requires at least 20% equity in your home and a good credit score.

- Home Equity Line of Credit (HELOC): A revolving credit line secured by your home's equity, typically available up to 65% of your home's value.

- Second mortgage: A separate loan that uses your home as collateral, allowing you to borrow up to 90% of your home's value when combined with your first mortgage.

The primary advantages of home equity solutions include:

- Lower interest rates: Secured loans typically offer significantly lower interest rates than credit cards and unsecured loans.

- Credit preservation: Unlike consumer proposals, these options don't necessarily damage your credit if payments are made on time.

- Tax deductibility: In some cases, interest on loans used for investments may be tax-deductible (consult a tax professional).

- Flexible repayment: Many equity products offer flexible repayment terms.

However, these options also come with considerations:

- Qualification requirements: You'll need sufficient equity, adequate income, and a reasonable credit score to qualify.

- Risk to your home: Using your home as collateral means it could be at risk if you can't make payments.

- Potential for higher total cost: Extending debt over a longer period may result in paying more interest overall.

For many homeowners, debt consolidation through home equity represents a less drastic alternative to a consumer proposal, particularly if you have good credit and sufficient equity. Services like Lotly offer home equity debt consolidation loans that can help you manage high-interest debts without the same credit consequences as formal insolvency proceedings.

Making the right decision for your financial future

Choosing between a consumer proposal, bankruptcy, or home equity solutions requires careful consideration of your unique financial situation. Here's a framework to help you evaluate your options:

The homeowner's debt relief decision framework

- Assess Your Equity Position:

- Calculate your home's current market value

- Subtract your mortgage balance

- The difference is your available equity (lenders typically allow borrowing up to 80% of your home's value minus your existing mortgage)

- Evaluate Your Debt-to-Income Ratio:

- Add up all monthly debt payments

- Divide by your monthly gross income

- If the result is over 43%, you may have difficulty qualifying for traditional refinancing

- Consider Your Credit Score:

- 680+ typically qualifies for conventional mortgage refinancing

- 600-680 may be eligible for B-lender options

- Below 600 may require alternative solutions, like a consumer proposal

- Analyze Your Debt Structure:

- Primarily unsecured debts (credit cards, personal loans) may benefit from either approach

- A mix of secured and unsecured debts might be better addressed through separate strategies

- Timeline Considerations:

- Need immediate relief from collection actions? A consumer proposal provides instant legal protection

- Planning to sell your home or refinance in the next 2-3 years? Home equity options may preserve more financial flexibility

When to seek professional help

Given the complexity and long-term implications of debt relief decisions, professional guidance is invaluable. Consider consulting with:

- Licensed Insolvency Trustee: For an assessment of whether a consumer proposal or bankruptcy is appropriate for your situation.

- Financial advisor: For a comprehensive review of your overall financial picture and long-term planning.

- Mortgage broker: To understand your home equity options and qualification likelihood.

- Credit counselor: For help with budgeting, money management, and non-insolvency debt solutions.

For homeowners specifically, services like Lotly provide personalized financial assessments with dedicated home financing advisors who can help you understand all available options. As fiduciaries, these advisors prioritize your best interests, ensuring you receive guidance tailored to your specific financial circumstances and goals.

Ready to take control of your debt with Lotly?

Taking steps to address overwhelming debt is a sign of financial responsibility, not failure. Whether a consumer proposal is right for you depends on your specific circumstances, including your home equity position, income stability, and long-term financial goals.

For many Canadian homeowners, the decision comes down to balancing immediate debt relief against long-term financial flexibility. Here are the key takeaways to consider:

- Consumer proposals offer significant debt reduction and legal protection while allowing you to keep your assets, but they impact your credit for several years.

- Home equity debt consolidation preserves your credit standing and may offer lower interest rates, but it requires sufficient equity and income qualification.

- The best solution depends on your unique situation, including your debt level, income stability, equity position, and future financial goals.

- Professional guidance from Licensed Insolvency Trustees, financial advisors, or home financing specialists can help you make an informed decision.

Remember that addressing debt proactively puts you in a stronger position than allowing the situation to deteriorate. Whether through a consumer proposal or home equity solution, taking action today can help secure your financial future and provide the peace of mind that comes with having a clear path forward.

P.S. — If you're a homeowner exploring your options, consider speaking with a home financing advisor who can help you understand how your home equity might be leveraged as an alternative to formal insolvency proceedings. With the proper guidance, you can find a solution that protects both your assets and your financial future.

Lotly provides secure home equity solutions for Canadian homeowners seeking a responsible alternative to insolvency. Even if you had a consumer proposal in the past, Lotly will be able to find a creative solution for your situation. Let our advisors help you consolidate debt, reduce stress, and confidently regain your financial footing.

Frequently Asked Questions

Can I keep my home if I file a consumer proposal?

Yes, you can keep your home in a consumer proposal as long as you continue making your mortgage payments. Unlike bankruptcy, a consumer proposal does not put your assets at risk.

How much does a consumer proposal cost?

There are no upfront costs to file a consumer proposal. The Licensed Insolvency Trustee's fees are regulated by the government and are included in your monthly payments.

Can creditors refuse my consumer proposal?

Yes, creditors can vote to reject your proposal if they believe it doesn't offer enough repayment. If this happens, your trustee can renegotiate the terms; alternatively, you may need to consider other options, such as bankruptcy.

Can I get a mortgage after a consumer proposal?

Yes, but it may be challenging until the proposal is completed and has been removed from your credit report. Some alternative lenders may consider applications sooner if you have a substantial down payment and stable income.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.