Summary

- Know what you're up against. While Canada has no direct "inheritance tax," the deemed disposition rules can trigger significant capital gains tax on appreciated assets at death.

- Use available exemptions strategically. From the principal residence exemption to spousal rollovers, these tools can dramatically reduce your estate's tax burden when properly applied.

- Consider your property options carefully. If you've inherited a home or own property, explore how secured home loans can help you access equity without selling cherished family assets.

- Don't go it alone. Estate planning involves complex tax, legal, and financial considerations—working with qualified professionals can save your estate thousands in unnecessary taxes and fees.

Your home holds memories, represents years of hard work, and might be your most valuable asset. But what happens to it—and all your other assets—when you're gone? While many Canadians worry about "inheritance tax" taking a big bite out of what they leave behind, the reality is more nuanced and often misunderstood.

In this comprehensive guide, you'll discover:

- The truth about what taxes actually apply when someone passes away in Canada

- Practical strategies to minimize the tax burden on your estate

- How to navigate provincial probate fees and federal tax obligations

P.S. — Lotly’s secured home loans give Ontario homeowners access to equity today—helping you cover taxes, probate fees, or debt obligations without diminishing family assets. If you’re a homeowner who needs cash to help plan your estate, get in touch with Lotly for a free consultation.

TL;DR

- No direct inheritance tax in Canada. Beneficiaries don't pay tax on inherited money or assets, but the estate may face significant tax obligations before distribution.

- Deemed disposition triggers capital gains. At death, assets are considered "sold" at fair market value, potentially creating taxable capital gains on the deceased's final tax return.

- Proper planning makes a difference. Strategic use of principal residence exemptions, spousal rollovers, and other techniques can significantly reduce the tax burden.

Does Canada have an inheritance tax?

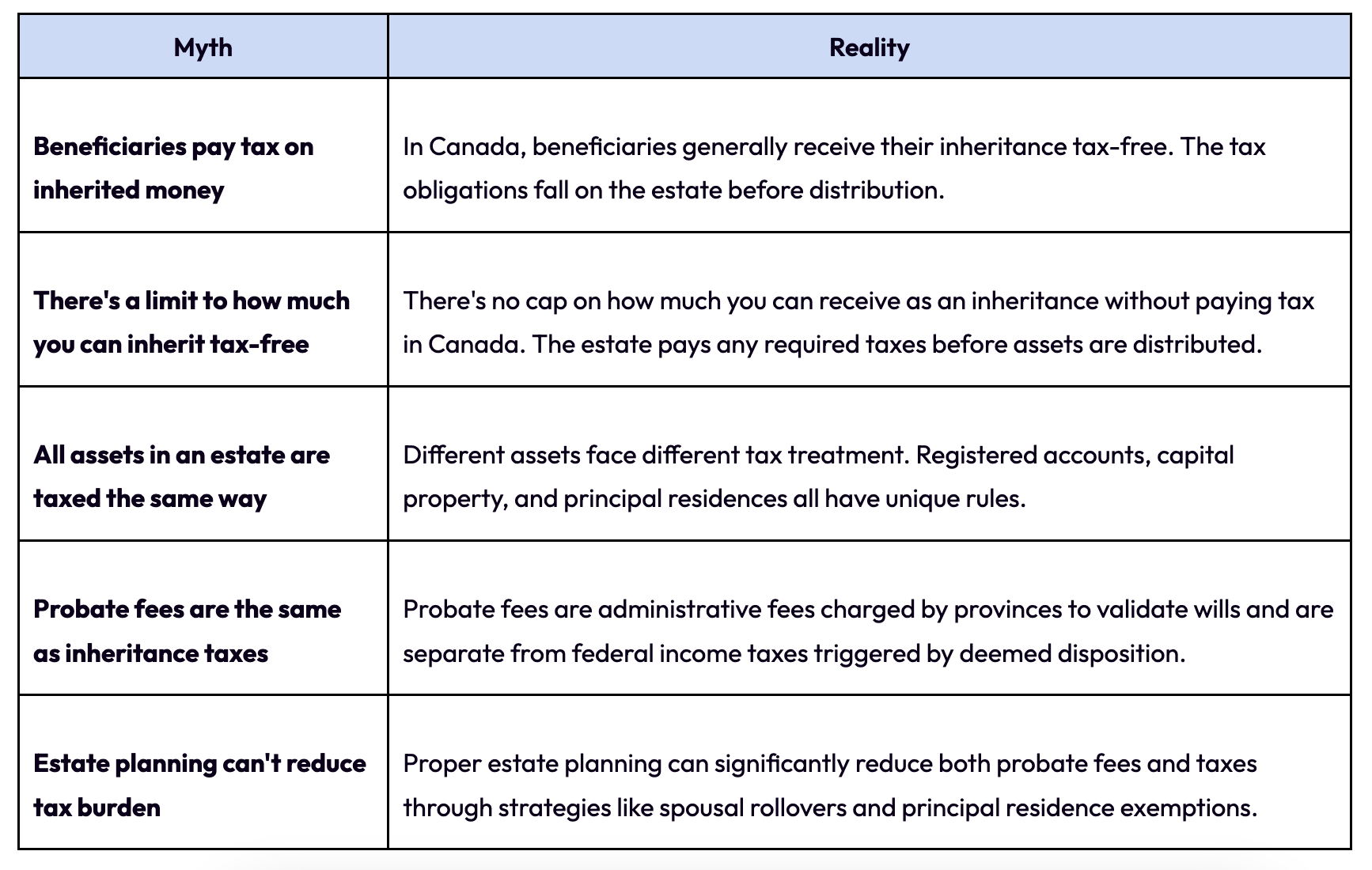

Canada does not have a direct inheritance tax or "death tax" that beneficiaries must pay when they receive assets from an estate. Unlike some countries where inheritors might pay tax on what they receive, in Canada, beneficiaries generally receive their inheritance tax-free.

However, this doesn't mean the assets escape taxation entirely. Instead, Canada uses a "deemed disposition" system that can trigger significant tax consequences for the estate before assets are distributed to beneficiaries. Understanding this system is crucial for effective estate planning.

When someone passes away in Canada, the Canada Revenue Agency (CRA) treats all capital property as if it were sold at fair market value immediately before death. This "deemed disposition" can trigger capital gains tax that must be paid by the estate before assets are distributed to beneficiaries.

How estates are taxed in Canada

The Canadian tax system treats death as a taxable event through several mechanisms. Here's what you need to know about how estates are taxed and what it means for your estate planning.

Deemed disposition at death

When a Canadian taxpayer dies, the CRA considers all their capital property to be "sold" at fair market value immediately before death. This deemed disposition applies to:

- Stocks, bonds, and mutual funds outside registered accounts

- Rental or investment properties

- Vacation properties

- Business assets

- Valuable collectibles and artwork

This means any increase in value (capital gain) from the time the asset was acquired until death becomes taxable on the deceased's final tax return.

How capital gains tax is calculated:

- Determine the fair market value of each asset at the time of death

- Subtract the adjusted cost base (original purchase price plus eligible costs)

- The difference is the capital gain

- Currently, 50% of capital gains are taxable (inclusion rate)

Example: If you purchased a cottage for $200,000 that's worth $500,000 when you pass away, the capital gain would be $300,000. At the current 50% inclusion rate, $150,000 would be added to your income in your final tax return and taxed at your marginal tax rate.

Important 2025 update: Beginning in 2026, individuals with annual capital gains exceeding $250,000 will have an increased inclusion rate of 66.67% (up from 50%) on the portion above $250,000. This change will affect high-value estates with significant unrealized capital gains.

Exceptions to deemed disposition rules:

- Assets transferred to a surviving spouse or common-law partner can use a tax-deferred rollover

- Qualified farm or fishing property may be eligible for special rollover provisions

- Principal residence may be exempt from capital gains tax

Tax on registered accounts (RRSPs, RRIFs, TFSAs)

Registered accounts receive different tax treatment at death:

RRSPs and RRIFs:

- By default, the fair market value of RRSPs and RRIFs is included as income on the deceased's final tax return

- This can result in a significant tax bill, as the entire value may be taxed at the highest marginal rate

- No capital gains calculation applies—the entire value is considered income

TFSAs:

- The value of a TFSA at death is not taxable

- Income earned in the TFSA after the date of death may be taxable to the beneficiary

- The TFSA contribution room is not transferable to non-spouse beneficiaries

Spousal rollover provisions:

When registered accounts are left to a surviving spouse or common-law partner, special rules apply:

- RRSPs/RRIFs: Can be transferred directly to the spouse's registered account without triggering immediate taxation

- TFSAs: If the spouse is named as a "successor holder," they can maintain the tax-free status of the account and assume ownership

Tax implications for non-spouse beneficiaries:

- RRSPs/RRIFs: The full value is included in the deceased's income for the year of death, and tax is paid by the estate

- TFSAs: The beneficiary receives the assets tax-free, but any growth after the date of death may be taxable

Principal residence exemption

One of the most valuable tax exemptions in Canada is the principal residence exemption, which can eliminate capital gains tax on your primary home:

- Each family unit can designate one property per year as their principal residence

- The exemption can eliminate capital gains tax on the designated property

- The exemption applies proportionally to the years the property was designated as a principal residence

How the principal residence exemption works at death:

- The executor must designate the property as a principal residence on the deceased's final tax return

- The exemption can eliminate or reduce capital gains tax on the property

- If transferred to a spouse, the property can maintain its status as a principal residence

For non-spouse beneficiaries:

- The property is deemed disposed of at fair market value at death

- The principal residence exemption can be claimed for the years the deceased owned and occupied the property

- The beneficiary's cost base becomes the fair market value at the date of death

Provincial probate fees across Canada

In addition to federal tax obligations, estates may also be subject to provincial probate fees. Probate is the legal process that validates a will and confirms the executor's authority to administer the estate.

Probate fees vary significantly by province and are calculated based on the estate's value. These fees are separate from federal income taxes and are paid to the provincial government.

Strategies to minimize probate fees

- Joint ownership with right of survivorship: Assets held jointly with right of survivorship pass directly to the surviving owner without going through probate.

- Beneficiary designations: Name specific beneficiaries on registered accounts (RRSPs, RRIFs, TFSAs) and life insurance policies so these assets pass outside the estate.

- Inter vivos trusts: Assets held in a trust established during your lifetime aren't considered part of your estate for probate purposes.

- Multiple wills: In some provinces, you can use multiple wills—one for assets that require probate and another for assets that don't.

- Gifting during lifetime: Assets given away during your lifetime won't be subject to probate fees (though tax implications should be considered).

Common misconceptions about inheritance tax in Canada

Many Canadians have misconceptions about how estates are taxed. Let's clear up some common myths:

Estate planning strategies to minimize tax burden

With proper planning, you can significantly reduce the tax burden on your estate. Here are some effective strategies to consider:

Gifting assets during your lifetime

Transferring assets to your intended beneficiaries while you're still alive can reduce the size of your estate and potentially lower both probate fees and taxes.

Benefits of lifetime gifting:

- Reduces the value of your estate subject to probate fees

- Allows you to see your beneficiaries enjoy your gifts

- May spread out capital gains over time rather than triggering them all at once

Tax considerations for gifting:

- Gifts to family members are generally not taxable in Canada

- Capital property is deemed disposed of at fair market value when gifted, potentially triggering immediate capital gains tax

- Cash gifts don't trigger capital gains tax

- Gifting to a spouse allows for a tax-deferred rollover

Documentation requirements:

- Keep records of all gifts, including dates, values, and recipients

- For substantial gifts, consider a formal gift letter or agreement

- For real property, ensure proper legal transfer documentation

Using trusts in estate planning

Trusts can be powerful tools for managing how your assets are distributed and potentially reducing tax burden.

Types of trusts relevant for Canadian estate planning:

- Testamentary trusts: Created through your will and take effect after death

- Can provide income-splitting opportunities for beneficiaries

- Subject to the highest marginal tax rate (except qualified disability trusts and graduated rate estates)

- Inter vivos trusts: Established during your lifetime

- Assets held in trust bypass probate

- Subject to the highest marginal tax rate

- 21-year deemed disposition rule applies

- Alter ego trusts: Available to individuals 65 or older

- Allow tax-deferred transfer of assets into the trust

- Assets bypass probate

- Deemed disposition occurs at death

- Joint partner trusts: Similar to an alter ego trust, but for couples

- Both spouses/partners must be 65 or older

- Deemed disposition occurs on the death of the second spouse

Tax advantages of different trust structures:

- Bypass probate fees

- Maintain privacy (unlike wills, which become public)

- Potential income splitting with beneficiaries

- Protection from creditors in some cases

When to consider setting up a trust:

- When you have substantial assets

- When you want to control how and when beneficiaries receive assets

- When you have beneficiaries with special needs

- When privacy is a concern

Joint ownership and beneficiary designations

Strategic use of joint ownership and beneficiary designations can help assets bypass probate and simplify estate administration.

Pros of joint ownership:

- Assets pass directly to the surviving joint owner without probate

- Immediate access to assets for the survivor

- Potential reduction in probate fees

Cons of joint ownership:

- Loss of control over the asset

- Potential immediate tax consequences when adding a joint owner

- Exposure to the joint owner's creditors

- Complications if the relationship deteriorates

Direct beneficiary designations:

- Available for registered accounts (RRSPs, RRIFs, TFSAs)

- Available for life insurance policies

- Assets pass directly to named beneficiaries outside the estate

- Not subject to probate fees

Potential pitfalls to avoid:

- Ensure beneficiary designations align with your will

- Consider contingent beneficiaries in case primary beneficiaries predecease you

- Be aware that jointly held assets may not be distributed according to your will

- Consider the tax implications for beneficiaries, especially for registered accounts

Life insurance strategies

Life insurance can be a valuable tool for covering estate tax liabilities and providing liquidity to your estate.

When using life insurance to cover estate tax liabilities:

- Policy proceeds can provide cash to pay taxes and probate fees

- Helps prevent forced sale of illiquid assets like real estate or businesses

- Proceeds paid directly to named beneficiaries bypass probate

Tax treatment of life insurance proceeds:

- Death benefits are generally received tax-free by beneficiaries

- Policy owned by a corporation may have different tax treatment

- Annual premiums are not tax-deductible for personal policies

Structuring policies for maximum tax efficiency:

- Consider an insurance trust to hold policy proceeds

- Ensure proper ownership structure (personal vs. corporate)

- Review beneficiary designations regularly

Cross-border inheritance tax considerations

If you have assets in other countries or beneficiaries who live abroad, cross-border tax issues can complicate your estate planning.

U.S.-Canada inheritance tax implications:

- U.S. citizens or residents may be subject to U.S. estate tax on worldwide assets

- The U.S. estate tax can apply to Canadian residents who own U.S. property

- The Canada-U.S. Tax Treaty provides some relief from double taxation

- The U.S. estate tax exemption is much higher than in previous years ($13.99 million in 2025)

Inheriting foreign property:

- May be subject to foreign inheritance or estate taxes

- Currency conversion issues can complicate valuation

- May require a foreign probate process

Tax treaties and foreign tax credits:

- Canada has tax treaties with many countries that may provide relief

- Foreign tax credits may be available to offset Canadian tax on foreign income

- Professional advice is essential for cross-border situations

Reporting requirements:

- Executors may need to file foreign tax returns

- Foreign assets may need to be reported to CRA

- Penalties for non-compliance can be severe

Using home equity after inheriting property

Inheriting property can present both opportunities and challenges. For those who inherit a home, accessing the equity can help manage inheritance-related expenses or achieve other financial goals.

Evaluating the inherited property's value and potential:

- Get a professional appraisal to establish its current market value

- Assess ongoing maintenance costs and property taxes

- Consider location, condition, and market trends

- Determine if the property has emotional significance

Financial considerations when deciding whether to keep or sell:

- Potential capital gains tax implications for non-principal residences

- Ongoing carrying costs (property taxes, maintenance, insurance)

- Opportunity cost of keeping illiquid equity tied up in the property

- Potential rental income if the property is suitable

Options for accessing equity in an inherited property:

If you decide to keep an inherited property but need access to some of the equity, several options are available:

- Traditional mortgage or refinancing

- Home equity line of credit (HELOC)

- Secured home loan

How secured home loans can help manage inheritance-related expenses:

For Ontario homeowners who've inherited property and need to access funds—whether for renovations, paying estate debts, or other purposes—Lotly's secured home loans offer a practical solution.

With Lotly's secured home loans, you can:

- Access between $10,000 and $1,000,000 based on your available equity

- Use funds to pay off estate debts, cover renovation costs, or consolidate existing debts

- Qualify regardless of your credit score or income type

- Typically receives funding within about two weeks once documents are submitted

This approach has helped many Ontario homeowners manage the financial aspects of inheritance while preserving family assets. Rather than selling an inherited property with sentimental value, a secured home loan allows you to access the equity while maintaining ownership.

Recent changes to Canadian tax laws affecting inheritances (2025)

Tax laws evolve, and staying informed about recent changes is crucial for effective estate planning. Here are the key updates for 2025 that could impact inheritances:

Updates to capital gains inclusion rates:

- Beginning in 2026, the capital gains inclusion rate will increase from 50% to 66.67% for annual capital gains exceeding $250,000

- This change will primarily affect estates with significant unrealized capital gains

- The standard 50% inclusion rate will continue to apply to capital gains below the $250,000 threshold

Changes to registered account rules:

- The Lifetime Capital Gains Exemption (LCGE) for qualifying small business shares, farm, or fishing property is increasing from $1,016,836 to $1,250,000 (effective June 25, 2024)

- This increase provides additional planning opportunities for business owners and farmers

Provincial probate fee adjustments:

- Most provinces have maintained their existing probate fee structures for 2025

- Always check with your provincial court for the most current fee schedule

Proposed legislation that could affect estate planning:

- The Department of Finance announced on January 31, 2025, that the increased capital gains inclusion rate for gains exceeding $250,000 will be deferred until January 1, 2026

- Monitor federal and provincial budgets for potential changes to tax laws affecting estates

Working with professionals on estate planning

Estate planning involves complex tax, legal, and financial considerations. Working with qualified professionals can help you develop a comprehensive plan that minimizes taxes and achieves your goals.

When to consult a tax professional:

- When you have significant assets or complex holdings

- When you own property in multiple jurisdictions

- When you have a business or professional practice

- When you're concerned about minimizing estate taxes

The role of estate lawyers:

- Drafting legally valid wills and powers of attorney

- Advising on probate and estate administration

- Creating trusts and other estate planning structures

- Ensuring your plan complies with relevant laws

Financial advisors and estate planning:

- Helping identify estate planning goals and priorities

- Recommending appropriate insurance and investment strategies

- Coordinating with other professionals (lawyers, accountants)

- Reviewing and updating plans as circumstances change

Costs vs. benefits of professional assistance:

- Professional fees are generally a small fraction of potential tax savings

- Proper planning can save thousands in taxes and probate fees

- Peace of mind knowing your affairs are in order

- Reduced burden on your executor and beneficiaries

Get a head start with Lotly

Understanding how Canada's tax system affects estates isn't just about saving money—it's about ensuring your hard-earned assets benefit the people and causes you care about. With the right strategies, you can significantly reduce the tax burden on your estate while creating a clear roadmap for your loved ones.

Here are your key takeaways:

- Know what you're up against. While Canada has no direct "inheritance tax," the deemed disposition rules can trigger significant capital gains tax on appreciated assets at death.

- Use available exemptions strategically. From the principal residence exemption to spousal rollovers, these tools can dramatically reduce your estate's tax burden when properly applied.

- Consider your property options carefully. If you've inherited a home or own property, explore how secured home loans can help you access equity without selling cherished family assets.

- Don't go it alone. Estate planning involves complex tax, legal, and financial considerations—working with qualified professionals can save your estate thousands in unnecessary taxes and fees.

P.S. — If you're an Ontario homeowner looking to access your home equity as part of your estate planning strategy, Lotly makes it simple. Our secured home loans offer flexible approval for all credit scores and income types, with transparent terms and a team that's on your side. Book a free consultation today to learn more.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.