Summary

- Focus on equipment value as your strongest asset when applying for financing with credit challenges – lenders care more about collateral than credit scores.

- Consider the hybrid collateral approach using secured home loans for equipment purchases, which can reduce interest rates by 2-4% compared to traditional bad credit equipment financing.

- Prepare comprehensive documentation before applying — organized and complete applications receive significantly faster approvals, even with credit challenges.

- Explore specialized lenders who understand your industry and equipment type rather than traditional banks with rigid credit requirements.

Looking for equipment financing, but worried your credit score will slam the door shut? You're not alone. While traditional lenders might turn you away, the reality is that equipment financing options exist specifically for businesses with credit challenges – often with surprisingly quick approval timelines.

In this comprehensive guide, we'll explore proven strategies for securing capital leasing with bad credit, including:

- Specialized lenders who focus on equipment value rather than just credit scores

- Documentation preparation that dramatically speeds up approval

- Alternative financing structures when traditional leasing isn't available

- The hybrid collateral approach that can significantly increase approval odds

P.S. — Lotly helps Ontario homeowners fund essential gear with secured home loans that welcome all credit scores and complex income, so your payments can actually align with cash flows. Book a no-pressure consultation today.

What is capital leasing and why does it work for bad credit?

Capital leasing represents a financing arrangement that allows businesses to acquire essential equipment while spreading payments over time. Unlike an operating lease (which functions more like a rental), a capital lease is structured with the intention of ownership transfer at the end of the term.

This financing structure works particularly well for businesses with credit challenges because the equipment itself serves as collateral, reducing the lender's risk. When evaluating your application, lenders know they can repossess and sell the equipment if payments aren't made – creating a natural security that increases approval odds, even with a poor credit history.

Key benefits of capital leasing for credit-challenged businesses include:

- Lower upfront costs – typically requires smaller down payments than purchasing outright

- Predictable monthly payments – helps with cash flow management and budgeting

- Potential tax advantages – lease payments may be deductible as business expenses

- Equipment serves as collateral – reducing the emphasis on perfect credit

- Builds business credit – on-time payments can improve your credit profile over time

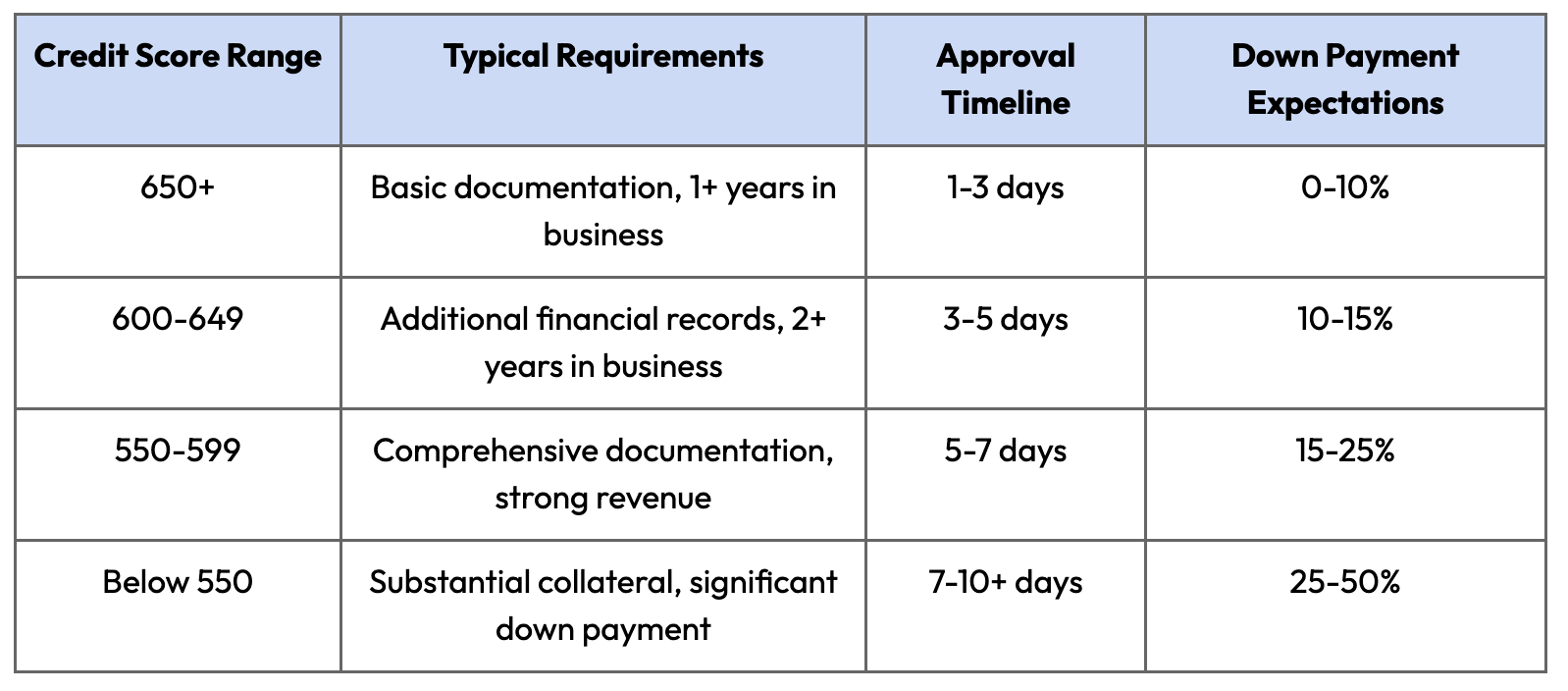

How bad credit affects capital lease approvals

Before diving into approval strategies, it's essential to understand how lenders evaluate businesses with credit challenges. Your credit score certainly matters, but it's just one piece of a more complex assessment.

Traditional lenders typically require minimum credit scores of 600-650 for equipment leasing, while alternative lenders may approve scores as low as 550 or even 500 in some cases. However, the lower your score, the more other factors come into play:

Beyond credit scores, lenders also evaluate:

- Time in business – longer operational history can offset credit concerns

- Monthly revenue – strong cash flow demonstrates repayment ability

- Industry stability – some sectors are considered lower risk than others

- Equipment type – essential, easily resalable equipment improves approval odds

- Existing debt load – your current debt-to-income ratio impacts approval

5 strategies for quick capital lease approval with bad credit

When your business needs equipment but your credit is less than perfect, these five strategies can significantly improve your chances of quick approval.

Focus on equipment value and collateralization

The equipment itself is your strongest asset when applying for capital leasing with bad credit. Lenders are far more likely to approve financing for essential, high-value equipment that holds its value and can be easily resold if necessary.

How to leverage equipment value effectively:

- Choose industry-standard equipment with proven resale markets rather than customized or niche machinery

- Document the equipment's useful life – longer-lasting equipment reduces depreciation risk

- Provide market comparisons showing the equipment's stable value retention

- Consider newer models – they typically have stronger collateral value than older versions

- Include maintenance records for used equipment to demonstrate condition

Pro Tip: When submitting your application, include photos, detailed specifications, and vendor quotes that highlight the equipment's value and its essential role in your business operations. This documentation helps lenders see the equipment as valuable collateral rather than focusing solely on your credit history.

Demonstrate strong cash flow

For lenders considering bad credit applications, proven cash flow often outweighs credit history. A business consistently generating substantial revenue presents a much lower risk, regardless of past credit issues.

Effective ways to showcase your cash flow:

- Prepare 3-6 months of bank statements showing consistent revenue

- Highlight upward trends in monthly income over time

- Create a cash flow projection demonstrating how the new equipment will impact revenue

- Document recurring revenue streams like subscriptions or service contracts

- Separate business and personal finances completely to show financial discipline

Documentation to strengthen your application:

- Recent bank statements (business and merchant accounts)

- Profit and loss statements for the past 6-12 months

- Current balance sheet showing assets and liabilities

- Sales forecasts that incorporate the new equipment

- Tax returns from the past two years

Offer a larger down payment

One of the most effective ways to address credit concerns is to offer a substantial down payment. This immediately reduces the lender's risk exposure and demonstrates your commitment to the investment.

Strategic down payment considerations:

- Industry standard – typical down payments for bad credit leasing range from 15-30%

- Sweet spot – increasing your down payment to 25-35% can significantly improve approval odds

- Break point – at approximately 40-50% down, many lenders will approve deals regardless of credit score

- ROI calculation – determine if the equipment's revenue generation justifies a larger upfront investment

Example down payment impact:

For a $50,000 piece of equipment:

- 10% down ($5,000) – May not be sufficient with bad credit

- 25% down ($12,500) – Substantially improves approval odds

- 40% down ($20,000) – Often secures approval even with severe credit issues

Pro Tip: If you can't afford a large down payment immediately, consider a 60-90 day deferred payment structure where you make a smaller initial payment followed by a balloon payment before the regular lease payments begin. This gives you time to generate revenue while still providing the lender with significant upfront security.

Choose specialized bad credit lenders

Not all equipment financing companies are created equal when it comes to bad credit situations. Specialized lenders who focus on subprime business financing often offer faster approvals and more flexible terms than traditional banks or general equipment financiers.

Characteristics of bad credit equipment lenders:

- Focus on collateral value rather than just credit scores

- Simplified documentation requirements designed for small businesses

- Industry specialization in specific equipment types

- Faster decision processes – often 24-48 hours versus weeks at traditional banks

- Higher approval rates for credit-challenged businesses

Types of specialized lenders to consider:

- Equipment-specific finance companies that understand the value and markets for particular machinery

- Alternative online lenders with streamlined digital application processes

- Captive financing arms of equipment manufacturers

- Local community banks with small business focus

- Credit unions with business lending programs

Prepare complete documentation

Nothing slows down the approval process more than incomplete paperwork. For quick approval with bad credit, your documentation must be comprehensive, accurate, and well-organized.

Essential documentation checklist:

- Business information:

- Business license and registration

- Articles of incorporation or organization

- EIN documentation

- Business plan summary (1-2 pages)

- Financial documentation:

- Last 6 months of bank statements

- Year-to-date profit and loss statement

- Balance sheet

- Last 2 years of business tax returns

- Personal tax returns for all owners (>20% ownership)

- Equipment documentation:

- Detailed equipment description and specifications

- Vendor quotes and purchase orders

- Photos of equipment (if used)

- Purpose and expected ROI of equipment

- Owner information:

- Government-issued ID

- Personal credit report (pulling your own prevents multiple inquiries)

- Resume showing industry experience

- Personal financial statement

Pro Tip: Create a single, organized PDF with all required documentation, complete with a table of contents and clear section dividers. This level of preparation signals professionalism and makes it easier for underwriters to review your application quickly.

Alternative financing options for equipment when you can’t lease

When traditional capital leasing isn't accessible due to credit challenges, several alternative financing structures can help you secure necessary equipment.

Secured home loans for business equipment

For business owners who own property, leveraging home equity can provide funding for equipment purchases when traditional financing isn't available. This approach is particularly effective for those with substantial home equity but challenging business credit profiles.

How it works with Lotly:

Lotly's secured home loans allow Ontario business owners to access funds ranging from $10,000 to $1,000,000 using their home equity as collateral. Unlike traditional equipment financing that focuses heavily on business credit scores, Lotly welcomes all credit scores and accepts all income types – including self-employed and side-gig income that many equipment lenders reject.

Key benefits for business equipment acquisition:

- Flexible approval criteria – All credit scores welcome, ideal for business owners with complex credit histories

- Quick funding timeline – Typically around 2 weeks from application to funding

- No restrictions on equipment type – Unlike direct equipment financing, funds can be used for any equipment needs

- Acceptance of all income types – Self-employed business owners welcome

- Cash-buyer advantage – Secure better equipment pricing as a cash buyer rather than a financing applicant

Want to make the vendor an all-cash offer? Use a Lotly secured home loan to purchase outright and negotiate better pricing.

Equipment rental with purchase options

Rent-to-own arrangements provide an alternative path to equipment ownership when traditional financing isn't available due to credit challenges.

How equipment rental-to-own works:

- Initial agreement – Start with a rental agreement for the equipment

- Monthly payments – A portion of each payment contributes toward eventual purchase

- Purchase option – After a specified period, exercise the option to buy at a predetermined price

- Ownership transfer – Equipment ownership transfers once final payment is made

Advantages compared to traditional leasing:

- Lower initial requirements – Often requires just the first and last month's payment

- Minimal credit checks – Many programs focus on cash flow rather than credit history

- Flexibility – Can return equipment if business needs change

- Try-before-you-buy – Test equipment performance before committing to ownership

- Tax benefits – Rental payments may be fully deductible as business expenses

Typical terms and conditions:

- Contract length: 12-36 months

- Monthly payment: 3-5% of equipment value

- Purchase option: 10-20% of the original value at the end of the term

- Early purchase discount: Many agreements offer a discounted buyout after 12 months

Vendor financing programs

Many equipment manufacturers and dealers offer their own financing programs, which often have more flexible credit requirements than third-party lenders.

Benefits of manufacturer financing:

- Industry-specific underwriting – Deep understanding of the equipment's value and use

- Relationship-based approval – May consider dealer relationships and purchase history

- Promotional rates – Special financing offers to move inventory

- Simplified process – One-stop shopping for equipment and financing

- Maintenance packages – Often include service agreements in the financing

How to access vendor financing with bad credit:

- Build a relationship with the dealer before applying for financing

- Demonstrate equipment expertise showing you'll properly maintain the asset

- Provide strong business references from suppliers and customers

- Consider certified pre-owned equipment which may have more flexible financing terms

- Negotiate a larger down payment to offset credit concerns

Industry-specific vendor programs:

- Construction equipment – Caterpillar, John Deere, and Komatsu offer financing for credit-challenged contractors

- Restaurant equipment – Suppliers like Sysco and US Foods provide equipment financing options

- Medical equipment – GE Healthcare and Philips offer specialized financing programs

- Transportation – Most major truck and vehicle manufacturers have captive financing arms

Invoice financing for equipment purchase

If your business has outstanding customer invoices, invoice financing (factoring) can provide immediate cash for equipment purchases regardless of your credit score.

How invoice financing works for equipment acquisition:

- Identify invoices – Select outstanding customer invoices from creditworthy clients

- Submit to factoring company – Provide invoice details and customer information

- Receive advance – Get 70-90% of invoice value upfront

- Purchase equipment – Use advanced funds for equipment acquisition

- Receive remainder – Get remaining funds (minus fees) when customer pays invoice

Advantages for bad credit situations:

- Based on customer credit – Your customers' creditworthiness matters more than yours

- Quick funding – Often within 24-48 hours

- No debt creation – Selling assets (invoices) rather than taking on new debt

- Scalable solution – Can factor more invoices as equipment needs grow

- No collateral required – The invoices themselves serve as the security

Typical costs and terms:

- Advance rate: 70-90% of invoice value

- Factor fee: 1-5% per 30 days (varies by industry and customer credit)

- Minimum volume: Many factors require at least $10,000 monthly invoice volume

- Contract terms: Can be as short as month-to-month

How to improve approval speed for capital leasing

When your business needs equipment quickly, these strategies can significantly accelerate the approval process – even with credit challenges.

Pre-qualification strategies

Before submitting formal applications, take these steps to identify suitable lenders and improve your approval odds:

- Credit profile review – Pull your business and personal credit reports to understand exactly what lenders will see

- Equipment research – Gather detailed specifications and market values for your desired equipment

- Lender matching – Use online marketplaces like Lendio or Equipment Finance Advisor to identify lenders who specialize in your situation

- Informal inquiries – Contact potential lenders for preliminary qualification criteria without triggering hard credit pulls

- Application preparation – Gather all required documentation before applying to prevent delays

Pro Tip: Create a one-page executive summary of your funding request that includes:

- Brief business description and time in operation

- Specific equipment needed and its purpose

- Monthly revenue and cash flow highlights

- Acknowledgment of credit challenges and compensating factors

- Proposed terms (down payment, desired monthly payment, term length)

This summary helps lenders quickly understand your situation and direct you to appropriate programs.

Documentation preparation checklist

Organize these documents in advance to prevent application delays:

Business Documentation:

- [ ] Business license and registration

- [ ] Articles of incorporation/organization

- [ ] EIN documentation

- [ ] Business bank statements (last 6 months)

- [ ] Profit and loss statement (year-to-date)

- [ ] Balance sheet (current)

- [ ] Business tax returns (last 2 years)

- [ ] Equipment quote or invoice

- [ ] Photos of equipment (if used)

- [ ] Business plan summary (1-2 pages)

Personal Documentation:

- [ ] Government-issued ID

- [ ] Personal credit report

- [ ] Personal tax returns (last 2 years)

- [ ] Personal financial statement

- [ ] Resume showing industry experience

Additional Supporting Materials:

- [ ] Customer contracts showing future revenue

- [ ] Existing equipment list and values

- [ ] Business debt schedule

- [ ] Explanation letter for past credit issues

- [ ] References from vendors or customers

Digital application platforms

Online application platforms can significantly accelerate the approval process:

- Equipment marketplace platforms like Lendio, Fundera, and National Business Capital allow you to submit one application to multiple lenders

- Direct lender portals from companies like Balboa Capital and Crest Capital offer streamlined digital applications

- Document upload systems with secure portals prevent email delays and security issues

- E-signature capabilities eliminate printing and mailing delays

- Mobile applications allow you to submit documents and check status from anywhere

Time-saving benefits:

- Automated document collection and verification

- Real-time application status updates

- Instant pre-qualification with some lenders

- Automated underwriting for faster decisions

- Digital contract execution

Common application mistakes that cause delays

Avoid these frequent errors that slow down the approval process:

- Incomplete applications – Missing fields or unsigned documents require follow-up

- Mismatched information – Discrepancies between the application and supporting documents raise red flags

- Outdated financial statements – Providing statements older than 60-90 days

- Unclear equipment specifications – Vague descriptions that require clarification

- Unrealistic terms – Requesting payment structures that don't align with industry standards

- Unexplained credit issues – Failing to address obvious credit problems proactively

- Missing business owner information – Applications without details for all owners with >20% stake

- Poor quality documentation – Illegible scans or photos of important documents

Pro Tip: Before submission, have someone unfamiliar with your business review your application package to identify any unclear or missing information. This fresh perspective often catches issues that could delay approval.

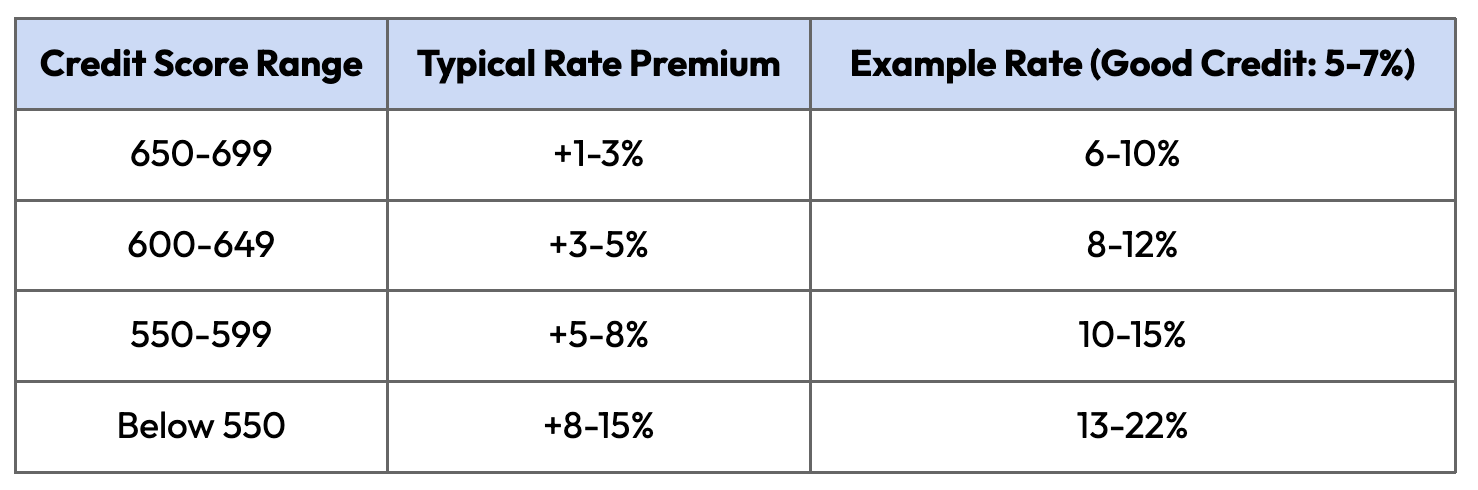

Understanding the true cost of bad credit capital leasing

When financing equipment with credit challenges, understanding the complete cost structure is essential for making informed decisions.

Rate premiums for bad credit leases

Credit challenges typically result in higher interest rates, but the specific premium varies by lender and situation:

Factors that can reduce rate premiums:

- Stronger down payment (25%+ of equipment value)

- Additional collateral beyond the equipment

- Strong business revenue despite credit issues

- Longer time in business (3+ years)

- Essential equipment with strong resale value

Fee structures and hidden costs

Beyond interest rates, be aware of these potential additional costs:

Typical fees in bad credit equipment leasing:

- Documentation fee: $100-$500 for processing paperwork

- Origination fee: 1-3% of the financed amount

- Credit investigation fee: $50-$150 for credit report and analysis

- UCC filing fee: $50-$100 for recording the security interest

- Insurance verification fee: $25-$75 for confirming coverage

- Late payment fees: Typically 5-10% of the payment amount

- Early termination fee: Often structured as a predetermined percentage of remaining payments

Hidden costs to watch for:

- Residual balloon payments at the end of the lease term

- Mandatory insurance with above-market premiums

- Automatic renewal clauses that extend the lease without explicit approval

- Maintenance requirements beyond normal care

- Return condition standards that may require significant investment

- Cross-collateralization clauses securing other business debts

Pro Tip: Request an amortization schedule and comprehensive fee disclosure before signing any agreement. Calculate the total cost of the lease over its entire term, including all fees and residual payments, to understand the actual cost of financing.

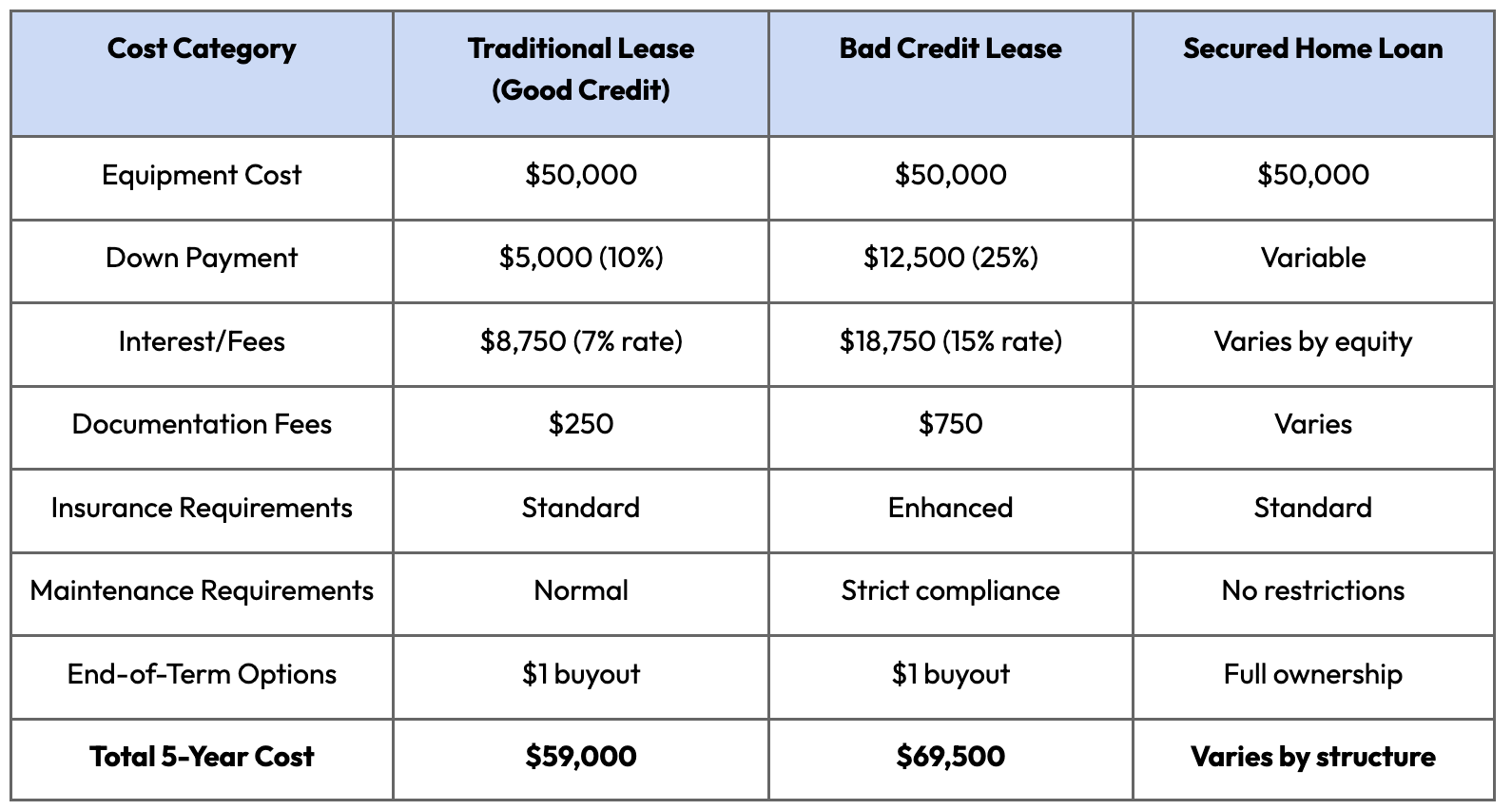

Total cost of ownership calculations

When evaluating equipment financing options, consider these factors beyond just the monthly payment:

Complete TCO formula: Total Cost = Purchase Price + Financing Costs + Maintenance + Insurance + Training + Downtime Costs - Residual Value

Example TCO comparison:

For a $50,000 piece of equipment over 5 years:

Strategies to reduce total cost despite credit challenges:

- Negotiate a shorter term – Higher payments but less total interest

- Make additional principal payments when cash flow allows

- Choose equipment with stronger residual value retention

- Consider certified pre-owned equipment with lower initial cost

- Evaluate the hybrid collateral approach using secured home loans for equipment purchases

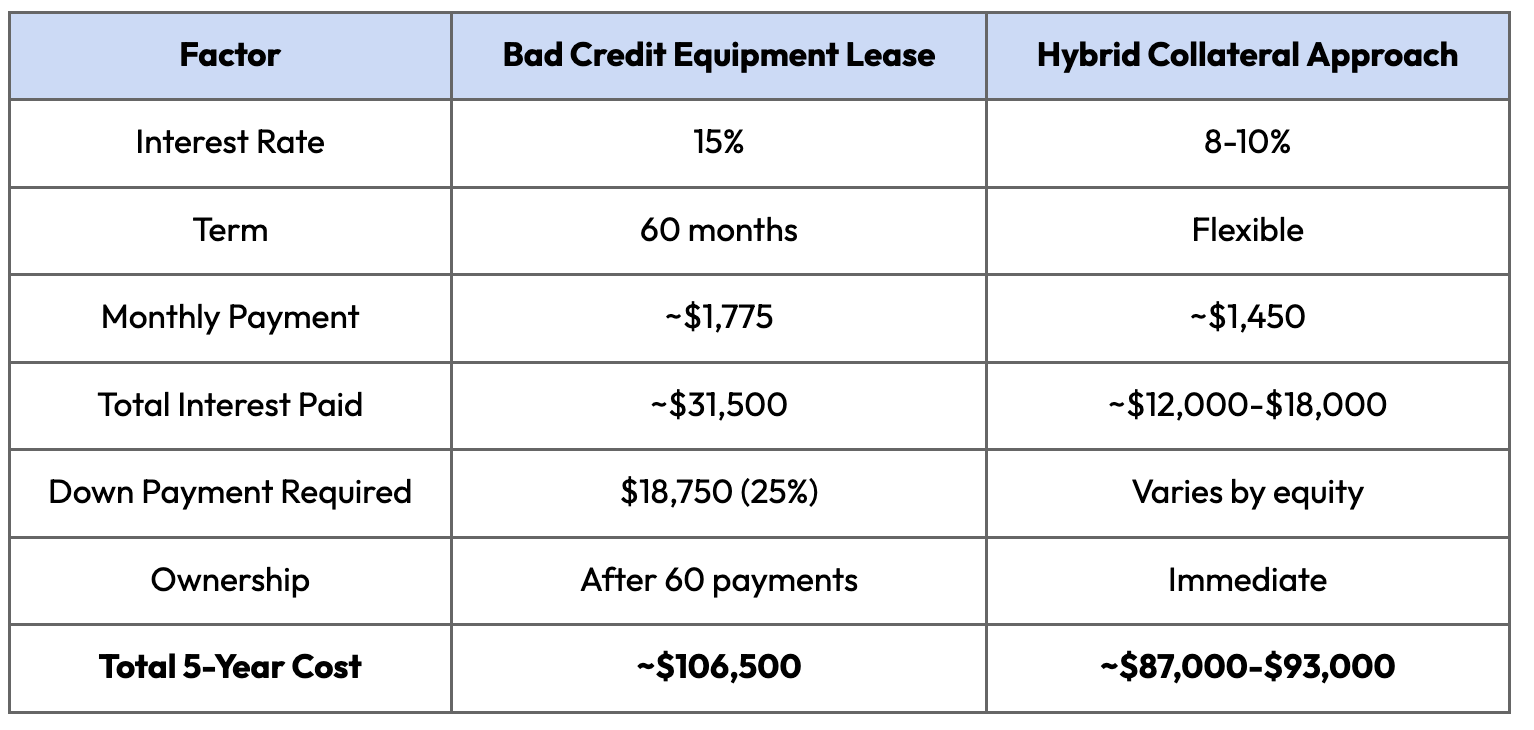

The hybrid collateral strategy for lower costs

For business owners who also own property, the hybrid collateral approach can significantly reduce financing costs despite credit challenges.

This strategy involves using a secured home loan (like those offered by Lotly) to purchase equipment outright rather than leasing. By leveraging real estate equity alongside the equipment's value, this approach creates a powerful dual-collateral position that often results in better terms than traditional bad credit equipment financing.

Cost advantages of the hybrid approach:

- Lower interest rates – Typically 2-4 percentage points below bad credit equipment leasing

- Reduced fees – Fewer documentation and origination charges

- No residual uncertainty – Full ownership from day one

- Flexible payment structures – Can be tailored to business cash flow

- Tax advantages – Potential for interest deductibility plus depreciation

Example cost comparison:

For a $75,000 equipment purchase:

Who benefits most from this approach:

- Business owners with sufficient home equity

- Those with complex income sources who traditional lenders reject

- Businesses needing multiple equipment pieces rather than a single asset

- Companies requiring faster funding than specialized equipment lenders can provide

Put your equipment plans in motion with Lotly

Securing equipment financing with credit challenges doesn't have to mean endless rejections or predatory terms. With the right approach – whether through specialized equipment lenders or alternative financing structures like Lotly's secured home loans – your business can access the equipment it needs to grow.

The key takeaways from our exploration of quick approval capital leasing with bad credit:

- Focus on equipment value as your strongest asset when applying for financing with credit challenges – lenders care more about collateral than credit scores.

- Consider the hybrid collateral approach using secured home loans for equipment purchases, which can reduce interest rates by 2-4% compared to traditional bad credit equipment financing.

- Prepare comprehensive documentation before applying — organized and complete applications receive significantly faster approvals, even with credit challenges.

- Explore specialized lenders who understand your industry and equipment type rather than traditional banks with rigid credit requirements.

If you're an Ontario homeowner running a business and need funds for equipment purchases, Lotly makes it simple. Our secured home loans accept a wide range of credit scores, accept all income types (including self-employed), and typically fund within about 2 weeks. Book a free consultation to see how you can get started today.

Frequently Asked Questions

What credit score do I need for equipment financing?

While traditional lenders typically require scores of 650+, specialized equipment lenders offer programs for scores as low as 550. Some lenders focus more on equipment value, time in business, and revenue than on credit scores. Alternative options like Lotly's secured home loans welcome all credit scores when business owners have sufficient home equity.

How long does it take to get equipment financing approval with bad credit?

Approval timelines vary by lender and situation, but specialized bad credit equipment lenders typically provide decisions within 2-7 business days. Online lenders and equipment marketplaces often offer the fastest approvals, sometimes within 24-48 hours. For the quickest funding, ensure your application is complete, your documentation is organized, and you're responsive to any lender questions.

What down payment is required for equipment financing with bad credit?

Down payment requirements typically range from 10%-50% based on your credit profile, with most bad credit situations requiring 20%-30%. The more challenged your credit, the larger the down payment needed. Offering a larger down payment (30% +) can significantly improve approval odds and secure better interest rates despite credit issues.

Can I get equipment financing if I've been rejected by banks?

Yes, specialized equipment lenders, alternative online lenders, and secured financing options like Lotly's home loans are specifically designed for businesses that don't qualify with traditional banks. These alternative funding sources consider factors beyond just credit scores, including equipment value, business revenue, and additional collateral options.

How can I improve my chances of equipment financing approval with bad credit?

Focus on demonstrating strong business fundamentals rather than dwelling on credit issues. Prepare detailed documentation showing consistent revenue, choose equipment with strong resale value, offer a substantial down payment (25%+), work with lenders specializing in your situation, and consider alternative structures, such as the hybrid collateral approach using secured home loans for equipment purchases.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.